Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Sea Limited (NYSE:SE) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

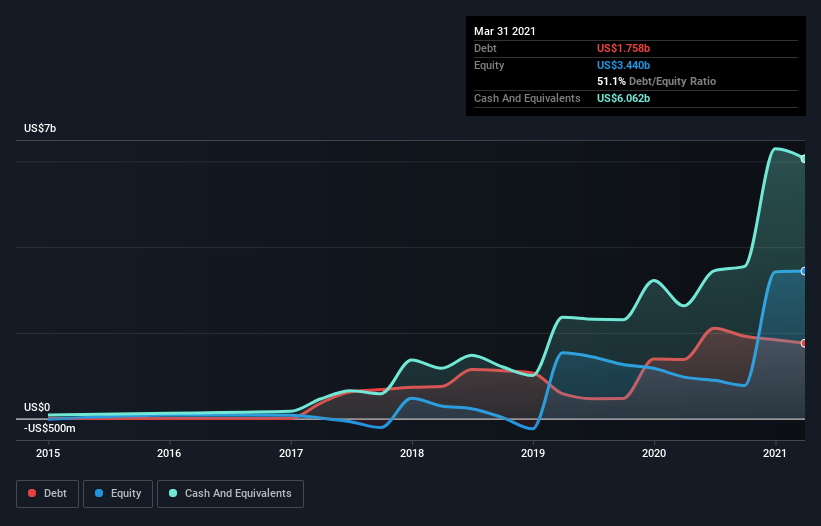

What Is Sea’s Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Sea had US$1.76b of debt, an increase on US$1.38b, over one year. But it also has US$6.06b in cash to offset that, meaning it has US$4.30b net cash.

A Look At Sea’s Liabilities

According to the last reported balance sheet, Sea had liabilities of US$5.08b due within 12 months, and liabilities of US$2.40b due beyond 12 months. Offsetting these obligations, it had cash of US$6.06b as well as receivables valued at US$795.4m due within 12 months. So its liabilities total US$624.5m more than the combination of its cash and short-term receivables.

Having regard to Sea’s size, it seems that its liquid assets are well balanced with its total liabilities. So while it’s hard to imagine that the US$143.5b company is struggling for cash, we still think it’s worth monitoring its balance sheet. While it does have liabilities worth noting, Sea also has more cash than debt, so we’re pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Sea can strengthen its balance sheet over time.

Over 12 months, Sea reported revenue of US$5.4b, which is a gain of 114%, although it did not report any earnings before interest and tax. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Sea?

While Sea lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$580m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. One positive is that Sea is growing revenue apace, which makes it easier to sell a growth story and raise capital if need be. But we still think it’s somewhat risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.