Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Equifax Inc. (NYSE:EFX) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Equifax’s Debt?

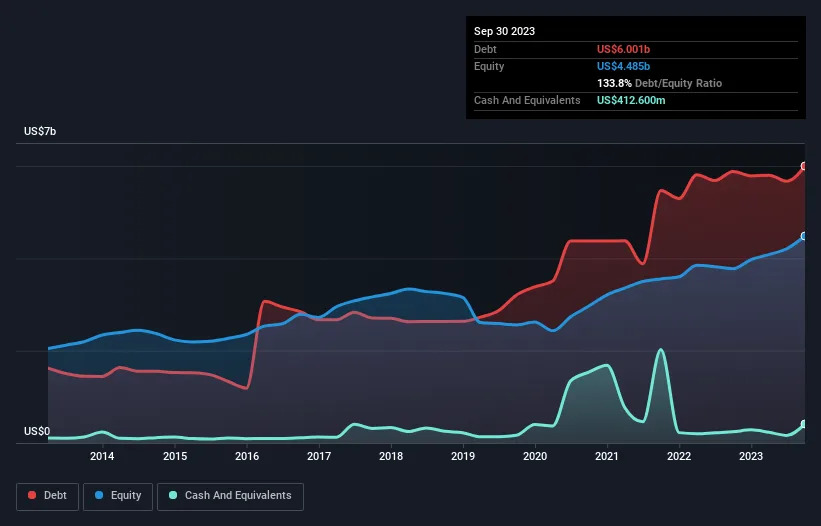

The chart below, which you can click on for greater detail, shows that Equifax had US$6.00b in debt in September 2023; about the same as the year before. However, because it has a cash reserve of US$412.6m, its net debt is less, at about US$5.59b.

How Strong Is Equifax’s Balance Sheet?

The latest balance sheet data shows that Equifax had liabilities of US$1.58b due within a year, and liabilities of US$6.28b falling due after that. Offsetting these obligations, it had cash of US$412.6m as well as receivables valued at US$996.6m due within 12 months. So its liabilities total US$6.46b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Equifax is worth a massive US$30.2b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Equifax’s debt is 3.7 times its EBITDA, and its EBIT cover its interest expense 3.8 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Even worse, Equifax saw its EBIT tank 21% over the last 12 months. If earnings keep going like that over the long term, it has a snowball’s chance in hell of paying off that debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Equifax’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Equifax recorded free cash flow of 49% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

We’d go so far as to say Equifax’s EBIT growth rate was disappointing. But at least its conversion of EBIT to free cash flow is not so bad. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Equifax stock a bit risky.