The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Quaker Chemical Corporation (NYSE:KWR) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Quaker Chemical Carry?

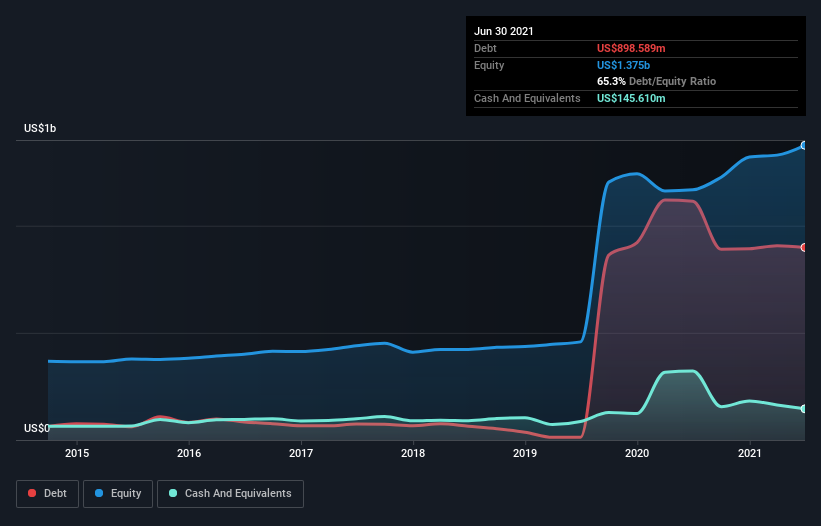

The image below, which you can click on for greater detail, shows that Quaker Chemical had debt of US$898.6m at the end of June 2021, a reduction from US$1.11b over a year. However, because it has a cash reserve of US$145.6m, its net debt is less, at about US$753.0m.

How Strong Is Quaker Chemical’s Balance Sheet?

The latest balance sheet data shows that Quaker Chemical had liabilities of US$400.4m due within a year, and liabilities of US$1.17b falling due after that. Offsetting this, it had US$145.6m in cash and US$418.6m in receivables that were due within 12 months. So it has liabilities totalling US$1.01b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Quaker Chemical has a market capitalization of US$4.69b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt to EBITDA of 2.8 Quaker Chemical has a fairly noticeable amount of debt. On the plus side, its EBIT was 8.4 times its interest expense, and its net debt to EBITDA, was quite high, at 2.8. Pleasingly, Quaker Chemical is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 101% gain in the last twelve months. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Quaker Chemical can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Quaker Chemical produced sturdy free cash flow equating to 69% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that Quaker Chemical’s demonstrated ability to grow its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its net debt to EBITDA does undermine this impression a bit. Looking at the bigger picture, we think Quaker Chemical’s use of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity. The balance sheet is clearly the area to focus on when you are analysing debt.