Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, The Kroger Co. (NYSE:KR) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Kroger’s Net Debt?

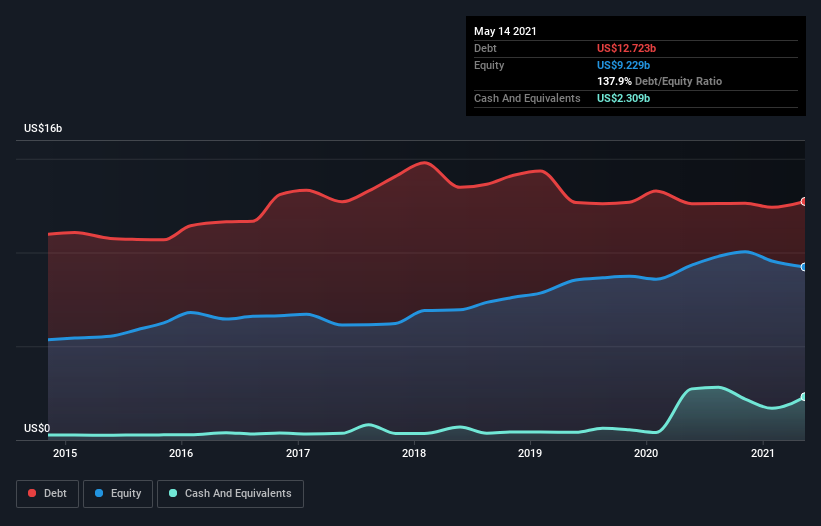

As you can see below, Kroger had US$12.7b of debt, at May 2021, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$2.31b, its net debt is less, at about US$10.4b.

A Look At Kroger’s Liabilities

Zooming in on the latest balance sheet data, we can see that Kroger had liabilities of US$15.2b due within 12 months and liabilities of US$24.4b due beyond that. Offsetting these obligations, it had cash of US$2.31b as well as receivables valued at US$1.94b due within 12 months. So its liabilities total US$35.3b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company’s massive market capitalization of US$34.4b, we think shareholders really should watch Kroger’s debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Kroger has net debt worth 1.9 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 5.0 times the interest expense. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. The bad news is that Kroger saw its EBIT decline by 17% over the last year. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Kroger can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Kroger produced sturdy free cash flow equating to 76% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

We’d go so far as to say Kroger’s EBIT growth rate was disappointing. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that Kroger’s debt is making it a bit risky. That’s not necessarily a bad thing, but we’d generally feel more comfortable with less leverage. The balance sheet is clearly the area to focus on when you are analysing debt.