Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Ormat Technologies, Inc. (NYSE:ORA) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Ormat Technologies Carry?

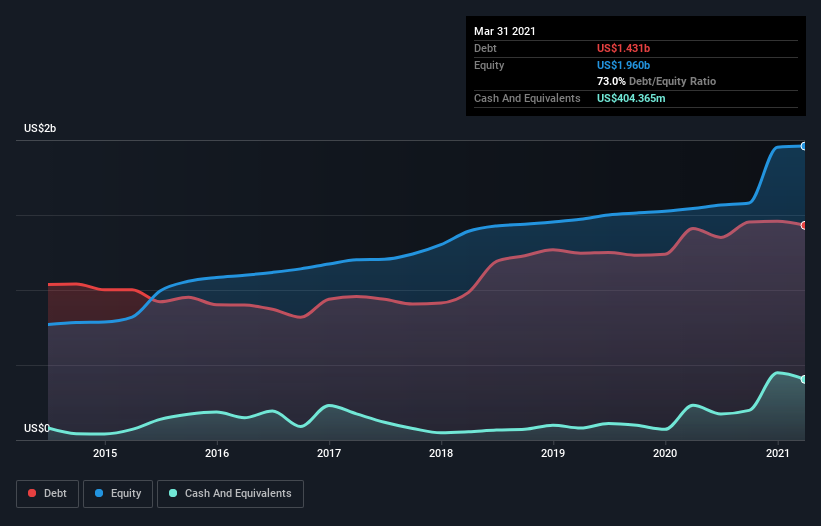

As you can see below, Ormat Technologies had US$1.43b of debt, at March 2021, which is about the same as the year before. You can click the chart for greater detail. However, it also had US$404.4m in cash, and so its net debt is US$1.03b.

NYSE:ORA Debt to Equity History June 30th 2021

A Look At Ormat Technologies’ Liabilities

The latest balance sheet data shows that Ormat Technologies had liabilities of US$254.2m due within a year, and liabilities of US$1.65b falling due after that. Offsetting these obligations, it had cash of US$404.4m as well as receivables valued at US$171.1m due within 12 months. So it has liabilities totalling US$1.32b more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Ormat Technologies is worth US$3.87b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn’t worry about Ormat Technologies’s net debt to EBITDA ratio of 2.9, we think its super-low interest cover of 2.4 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. More concerning, Ormat Technologies saw its EBIT drop by 4.7% in the last twelve months. If it keeps going like that paying off its debt will be like running on a treadmill — a lot of effort for not much advancement. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Ormat Technologies’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Ormat Technologies saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Mulling over Ormat Technologies’s attempt at converting EBIT to free cash flow, we’re certainly not enthusiastic. Having said that, its ability to handle its total liabilities isn’t such a worry. Overall, we think it’s fair to say that Ormat Technologies has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.