David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Eastman Kodak Company (NYSE:KODK) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Eastman Kodak’s Debt?

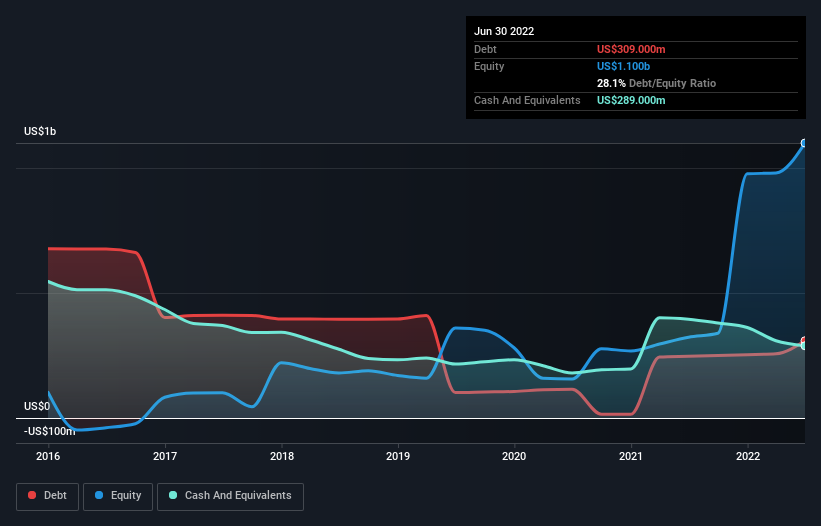

As you can see below, at the end of June 2022, Eastman Kodak had US$309.0m of debt, up from US$247.0m a year ago. Click the image for more detail. However, it does have US$289.0m in cash offsetting this, leading to net debt of about US$20.0m.

How Healthy Is Eastman Kodak’s Balance Sheet?

According to the last reported balance sheet, Eastman Kodak had liabilities of US$318.0m due within 12 months, and liabilities of US$891.0m due beyond 12 months. Offsetting these obligations, it had cash of US$289.0m as well as receivables valued at US$192.0m due within 12 months. So it has liabilities totalling US$728.0m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$359.6m company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Eastman Kodak would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Eastman Kodak has a very low debt to EBITDA ratio of 0.22 so it is strange to see weak interest coverage, with last year’s EBIT being only 1.6 times the interest expense. So one way or the other, it’s clear the debt levels are not trivial. If Eastman Kodak can keep growing EBIT at last year’s rate of 20% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But it is Eastman Kodak’s earnings that will influence how the balance sheet holds up in the future.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Eastman Kodak burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Eastman Kodak’s conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its net debt to EBITDA is a good sign, and makes us more optimistic. Overall, it seems to us that Eastman Kodak’s balance sheet is really quite a risk to the business. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say.