Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that NeoGenomics, Inc. (NASDAQ:NEO) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does NeoGenomics Carry?

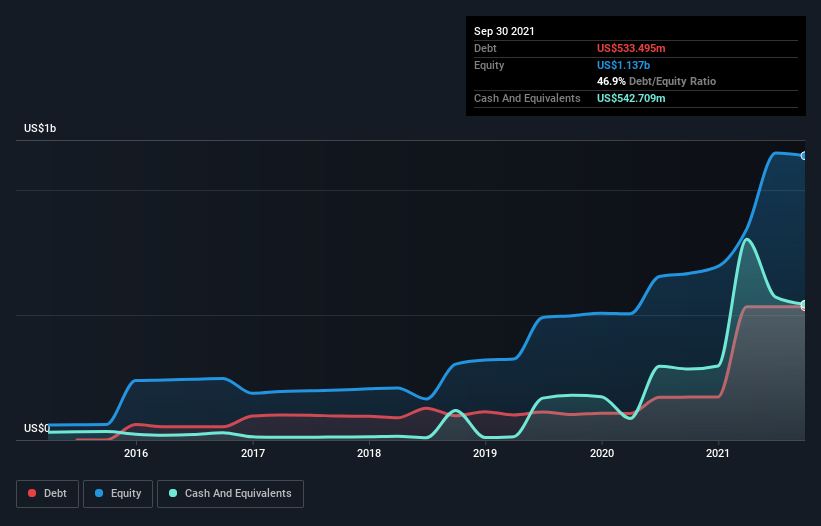

You can click the graphic below for the historical numbers, but it shows that as of September 2021 NeoGenomics had US$533.5m of debt, an increase on US$171.5m, over one year. However, its balance sheet shows it holds US$542.7m in cash, so it actually has US$9.21m net cash.

A Look At NeoGenomics’ Liabilities

Zooming in on the latest balance sheet data, we can see that NeoGenomics had liabilities of US$92.7m due within 12 months and liabilities of US$676.4m due beyond that. On the other hand, it had cash of US$542.7m and US$107.4m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$119.1m.

Given NeoGenomics has a market capitalization of US$3.58b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, NeoGenomics also has more cash than debt, so we’re pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if NeoGenomics can strengthen its balance sheet over time.

In the last year NeoGenomics wasn’t profitable at an EBIT level, but managed to grow its revenue by 14%, to US$485m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is NeoGenomics?

While NeoGenomics lost money on an earnings before interest and tax (EBIT) level, it actually booked a paper profit of US$49m. So when you consider it has net cash, along with the statutory profit, the stock probably isn’t as risky as it might seem, at least in the short term. With revenue growth uninspiring, we’d really need to see some positive EBIT before mustering much enthusiasm for this business. The balance sheet is clearly the area to focus on when you are analysing debt.