Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies U.S. Silica Holdings, Inc. (NYSE:SLCA) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does U.S. Silica Holdings Carry?

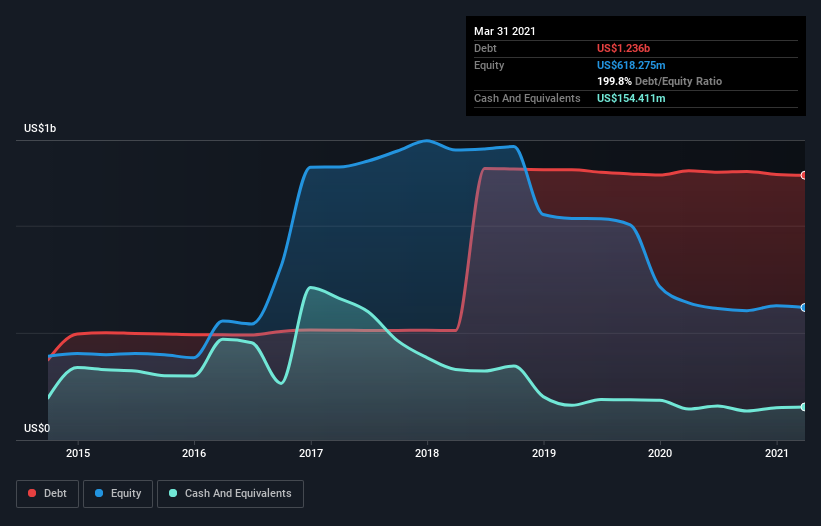

As you can see below, U.S. Silica Holdings had US$1.24b of debt, at March 2021, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$154.4m in cash leading to net debt of about US$1.08b.

How Healthy Is U.S. Silica Holdings’ Balance Sheet?

The latest balance sheet data shows that U.S. Silica Holdings had liabilities of US$197.9m due within a year, and liabilities of US$1.40b falling due after that. Offsetting this, it had US$154.4m in cash and US$211.8m in receivables that were due within 12 months. So it has liabilities totalling US$1.23b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$765.7m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, U.S. Silica Holdings would probably need a major re-capitalization if its creditors were to demand repayment. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if U.S. Silica Holdings can strengthen its balance sheet over time.

In the last year U.S. Silica Holdings had a loss before interest and tax, and actually shrunk its revenue by 41%, to US$811m. That makes us nervous, to say the least.

Caveat Emptor

While U.S. Silica Holdings’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost US$1.1m at the EBIT level. When we look at that alongside the significant liabilities, we’re not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. It’s fair to say the loss of US$63m didn’t encourage us either; we’d like to see a profit. In the meantime, we consider the stock to be risky. There’s no doubt that we learn most about debt from the balance sheet.