Renault (OTC:RNSDF) is setting the stage for a flow of significant news in May. Expect a re-commitment to its Japanese Alliance via a cost-saving plan and detailed Nissan (OTCPK:NSANY) restructuring, coupled with a plan to reduce operating fixed costs at its core business. With the current share price seeming to focus on accounting EPS numbers rather than the group’s cash flow generation, effective implementation of these measures could prove a catalyst for share price performance from here. Furthermore, with the recent market turmoil bringing the Renault stub valuation into significantly negative territory despite a well-capitalized balance sheet, I would be a buyer at these levels.

Reviewing the 2019 Results

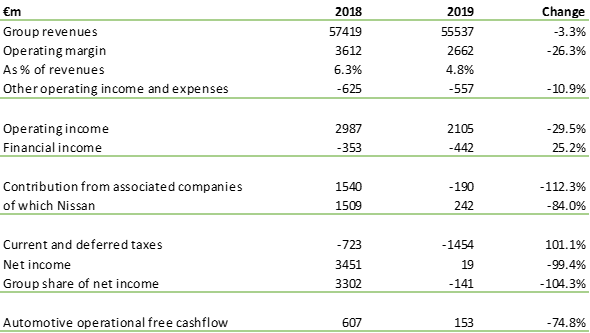

Per Renault’s latest results, group revenues declined by 3.3%. This was largely due to a combination of lower volumes, particularly in Argentina, Turkey (where currency devaluation also negatively effected figures) and Algeria. Sales to partners also declined, although there was a positive impact from prices in Europe, where a more robust pricing policy was implemented.

The group operating margin decreased by 26% to €2.67 billion, some €100 million below consensus, with a much weaker second half, explained by investment in product enrichment not being passed on to customer pricing. Automotive operating margin (excluding AVTOVAZ) fell to €1.28 billion, now representing just 48% of the group total.

Table 1: Key result parameters, 2018-2019

Free cash flow was marginally positive (€150 million) due to a positive change in working capital requirements (specifically movements in leased vehicles) and an increase in dividends received from RCI Banque (Renault’s financing arm). However, the quality of these results is questionable, given that 54% of R&D is capitalized. Additionally, the significant €1.0 billion positive change in working capital was difficult to predict. Excluding the dividend from RCI and the exceptional working capital change, free cash flow was negative to the tune of €1.0 billion – a hefty sum.

Further visibility on plans for electric vehicles

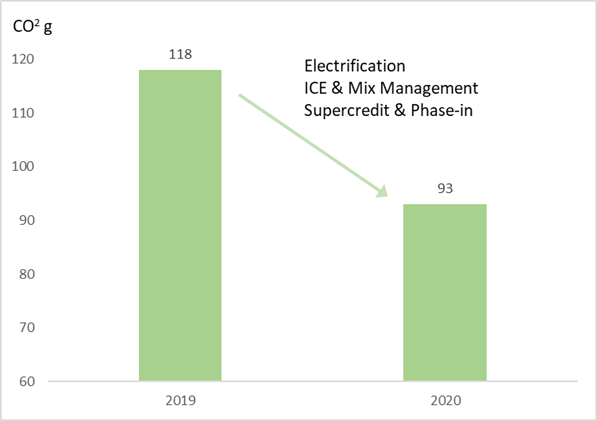

In terms of the electrification of its range, Renault anticipates a sales mix with 10% BEV and PHEV (Battery and Plug-in Hybrid) vehicles, 30% HEV (Hybrid) and Diesel, 10% LPG and 50% internal combustion engines (ICE) in 2020. BEVs are expected to represent the majority of the BEV/PHEV category and Diesel the majority of the Hybrid/Diesel category. The main increases will come through the BEV/PHEV and LPG segments (the latter largely through the Dacia brand). Achieving this sales mix, along with a significant increase in the efficiency of its ICE engines, should enable Renault to reduce the group’s average CO2 emission per km per vehicle from 118g in 2019 to 93g in 2020 (Chart 1) and to achieve regulatory compliance with more ease relative to its German peers.

Renault is uniquely positioned on its BEVs given that it moved earlier to produce BEVs than any other European OEM, allowing it to secure its supply chain. Renault sold over 40,000 “Zoe” cars in 2019 and plans to sell c100,000 in 2020 (10,000 have already been sold in January). Interestingly, 50% of “Zoes” are being sold in more rural areas, and 80% of charging is happening at home or destination. This is critical given France’s poor public charging infrastructure.

Chart 1: Planned CO2 emission per km per vehicle reduction

2020 Outlook

I am downbeat on the margin profile, partly due to a lack of topline growth and partly due to incremental costs (not passed along to customers). Since depreciation will increase by an equivalent amount, it should have no impact on cash flow. For Renault (and the industry as a whole), 2020 is likely to be a very complicated year, especially in Europe, given ambitious CO2 targets.

Renault guides cautiously for markets in 2020, with shrinkage in Europe at -3% and Russia -3%, but further expansion in Brazil +5%. It also expects flat revenues on the annual comparison despite these weaker markets, which could prove slightly optimistic. Group EBIT margins are expected to come in at 3-4% for FY20, weaker than I had hoped, and extrapolating roughly the 2H19 achievement. The guidance also points to a further positive automotive free cash flow for FY20, which should be achievable from working capital changes.

Revenues: Two-thirds of revenues are likely to be derived from Europe in 2020 (52% of volumes) and the remainder from outside the continent. In a weak European market, the group should benefit from the renewal of its entire B segment, or 60% of its line-up (mostly Clio, Zoe, Captur, Sandero, and Kangoo). This should enable it to achieve a firmer pricing environment and potentially boost volumes too. The success of electrification in this segment is likely to be a challenge, though, as it will likely be for all other OEMs. Renault targets 10% of BEV + PHEVs (or 200,000 units in Europe) and 10% LPG (mostly for the Dacia line-up, which should benefit from lower CO2 emissions). I also expect lower revenues from sales to partners.

Operating Margin: Given a small increase in the contribution from RCI, this implies the auto division should generate an operating margin of a meager 1%. This is after: i) €500 million of additional depreciation; ii) €500 million of additional mix enrichment (or 2x more than that of 2019); and, iii) €400 million of cost savings. This assumes that all earnings drivers (raw materials, volume, and forex, etc.) have a relatively neutral impact on operating profit.

Free Cash Flow: Cash flow should be comparable to 2019 (lower results offset by higher depreciation), in my view. To generate positive free cash flow ex restructuring, the group will need a strong dividend from RCI (€500 million) and a positive change in working capital, close to that achieved in 2019 (€1.0 billion).

Balance Sheet Concerns Overdone

Renault’s automotive net liquidity at FY19 was €1.7 billion, better than expected, with the €1.97 billion decline due to the FY19 dividend paid of €3.55 per share, the IFRS16 impact, changes in the consolidation scope and investments in mobility and autonomous driving. The auto division also highlighted over €15.8 billion in accessible cash and liquidity reserves. Guidance is for further positive auto free cash flow in FY20, suggesting that the balance sheet, though weaker than peers, remains adequate for now.

Furthermore, Renault clearly has the potential for dividends from RCI Banque and asset disposals, as highlighted. In my view, the company has managed with a similar balance sheet for many years, and thus, there is no basis to believe that needs to change now. I think the balance sheet concerns are significantly overdone.

Key Events in May

On a positive note, Renault is taking action with those matters it can best control. The company seeks to remove circa €2 billion from its fixed cost base (implying a 20% reduction) in the next three years. This will be taken out from, for example, general and administrative costs, marketing, and non-core disposals, with plans to be further refined and presented at a Capital Markets Day in May. Additionally, acting CEO Delbos made positive noises on cohesion in the Alliance, with further details again planned for May, refreshingly pointing out the need for action.

The significance of this fixed cost reduction is emphasized by the fact that it involves the closure of assembly plants, given five (of which three are in France) now run at or less than 50% capacity, and workforce adjustments (140,000 employees ex AVTOVAZ, of which 50% are in Europe). This could then be a rocky ride given the strength of French unions. Notably, too, the detailed revelation of this plan and the re-invigoration of the Alliance will occur two months before the arrival of Mr. Luca de Meo, the new CEO. Time will tell whether he buys into all of it or strives to make his mark on the group’s evolution.

Entering Deep Value Territory

Excluding the 43% stake in Nissan and the 2% stake in Daimler, the core business of Renault’s equity value appears to have sunk to new lows – at current levels, the company’s core business (including RBI) is being valued at a significant negative valuation, by my estimates.

Euro (million) | |

| Market cap (296 million shares @ share price) | 4,834 |

| Net cash (Dec ’19e) | (2,470) |

| Pension liabilities (Dec ’18) | 1,531 |

| Renault Group EV | 3,895 |

| Euro (million) | Price | |||

| 1830 million Nissan shares @s/price | 5536 | 363 | Nissan value / Renault share | € 19 |

| 14 million Daimler shares @ s/price | 351 | 25 | Daimler value/ Renault share | € 1 |

| EV of Renault core (by difference) | (1,992) | Renault core by difference | -€ 4 | |

| 3,895 | Current Price | € 16 |

Current valuations represent a new low for the Renault stub valuation despite a stronger balance sheet today than over the last 20 years. Overall, while the EBIT performance in 2019 was disappointing as well as guidance into 2020, I think Renault is well-positioned on CO2 compliance. Demand is strong for the “Zoe”, and the company is already breakeven on the car. The proposed fixed cost reductions will also undoubtedly benefit margins.

Further, Renault has €13 billion in automotive cash on its balance sheet and can support itself without a Nissan dividend, yet it continues to trade at a negative enterprise value when incorporating Nissan’s public equity. I continue to believe that a resolution of this dynamic, which may occur through either a merger or sell-down of the Nissan stake, would be a catalyst for the shares. Furthermore, improving conditions at Renault’s core operations would be met favorably by investors. Actions speak louder than words.