Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Ionis Pharmaceuticals, Inc. (NASDAQ:IONS) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Ionis Pharmaceuticals’s Net Debt?

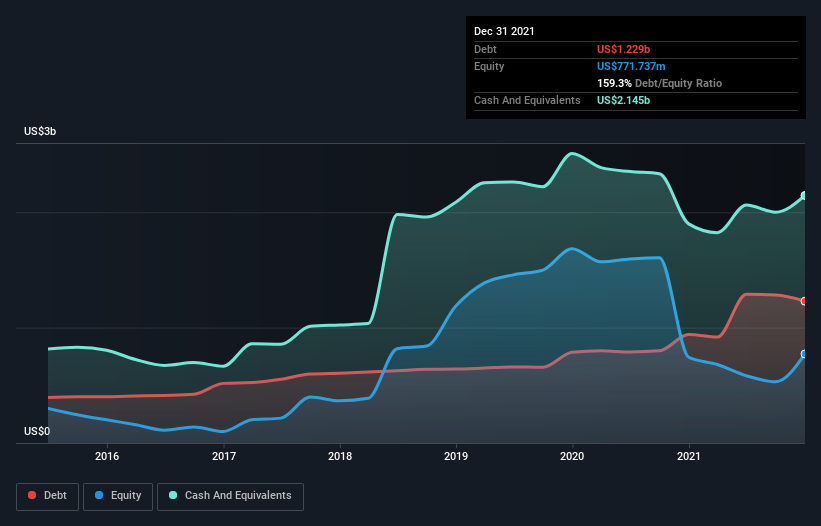

The image below, which you can click on for greater detail, shows that at December 2021 Ionis Pharmaceuticals had debt of US$1.23b, up from US$939.6m in one year. But on the other hand it also has US$2.15b in cash, leading to a US$916.1m net cash position.

How Healthy Is Ionis Pharmaceuticals’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Ionis Pharmaceuticals had liabilities of US$240.6m due within 12 months and liabilities of US$1.60b due beyond that. Offsetting this, it had US$2.15b in cash and US$61.9m in receivables that were due within 12 months. So it can boast US$367.0m more liquid assets than total liabilities.

This surplus suggests that Ionis Pharmaceuticals has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Ionis Pharmaceuticals has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Ionis Pharmaceuticals’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Ionis Pharmaceuticals reported revenue of US$810m, which is a gain of 11%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Ionis Pharmaceuticals?

Although Ionis Pharmaceuticals had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$13m. So taking that on face value, and considering the net cash situation, we don’t think that the stock is too risky in the near term. With mediocre revenue growth in the last year, we’re don’t find the investment opportunity particularly compelling. When analysing debt levels, the balance sheet is the obvious place to start.