David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Ingles Markets, Incorporated (NASDAQ:IMKT.A) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Ingles Markets Carry?

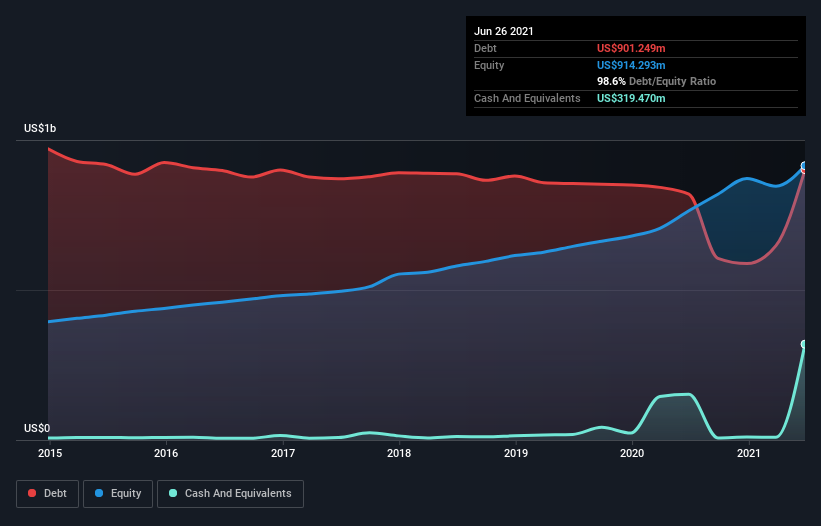

As you can see below, at the end of June 2021, Ingles Markets had US$901.2m of debt, up from US$819.3m a year ago. Click the image for more detail. However, because it has a cash reserve of US$319.5m, its net debt is less, at about US$581.8m.

How Strong Is Ingles Markets’ Balance Sheet?

According to the last reported balance sheet, Ingles Markets had liabilities of US$585.6m due within 12 months, and liabilities of US$747.6m due beyond 12 months. Offsetting this, it had US$319.5m in cash and US$90.2m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$923.6m.

This is a mountain of leverage relative to its market capitalization of US$1.53b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Ingles Markets’s net debt is only 1.2 times its EBITDA. And its EBIT easily covers its interest expense, being 13.1 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. In addition to that, we’re happy to report that Ingles Markets has boosted its EBIT by 55%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But you can’t view debt in total isolation; since Ingles Markets will need earnings to service that debt. So when considering debt, it’s definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Ingles Markets produced sturdy free cash flow equating to 56% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Happily, Ingles Markets’s impressive interest cover implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its level of total liabilities. Taking all this data into account, it seems to us that Ingles Markets takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. When analysing debt levels, the balance sheet is the obvious place to start.