Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Insperity, Inc. (NYSE:NSP) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Insperity’s Net Debt?

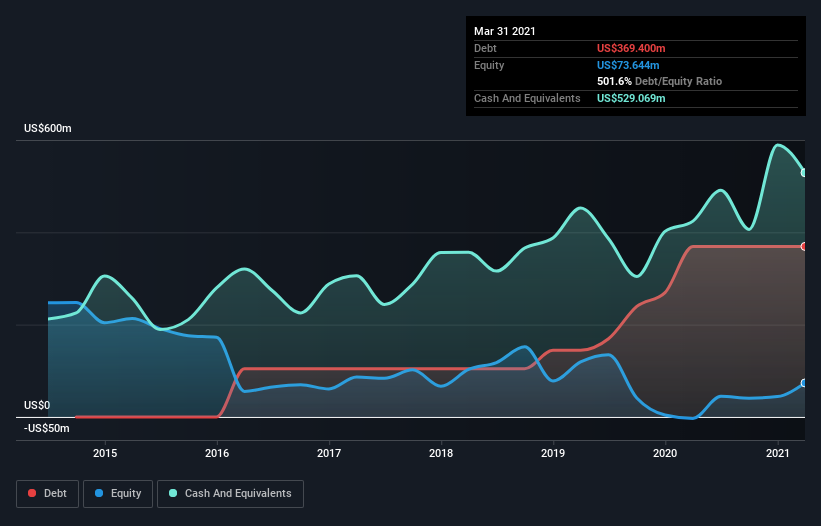

As you can see below, Insperity had US$352.9m of debt at March 2021, down from US$369.4m a year prior. But on the other hand it also has US$529.1m in cash, leading to a US$176.2m net cash position.

How Strong Is Insperity’s Balance Sheet?

We can see from the most recent balance sheet that Insperity had liabilities of US$1.04b falling due within a year, and liabilities of US$651.1m due beyond that. Offsetting this, it had US$529.1m in cash and US$564.7m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$601.7m.

Given Insperity has a market capitalization of US$3.62b, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Insperity also has more cash than debt, so we’re pretty confident it can manage its debt safely.

The good news is that Insperity has increased its EBIT by 3.7% over twelve months, which should ease any concerns about debt repayment. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Insperity’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Insperity may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Insperity generated free cash flow amounting to a very robust 88% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Summing up

While Insperity does have more liabilities than liquid assets, it also has net cash of US$176.2m. And it impressed us with free cash flow of US$230m, being 88% of its EBIT. So we don’t think Insperity’s use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.