Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies HyreCar Inc. (NASDAQ:HYRE) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is HyreCar’s Debt?

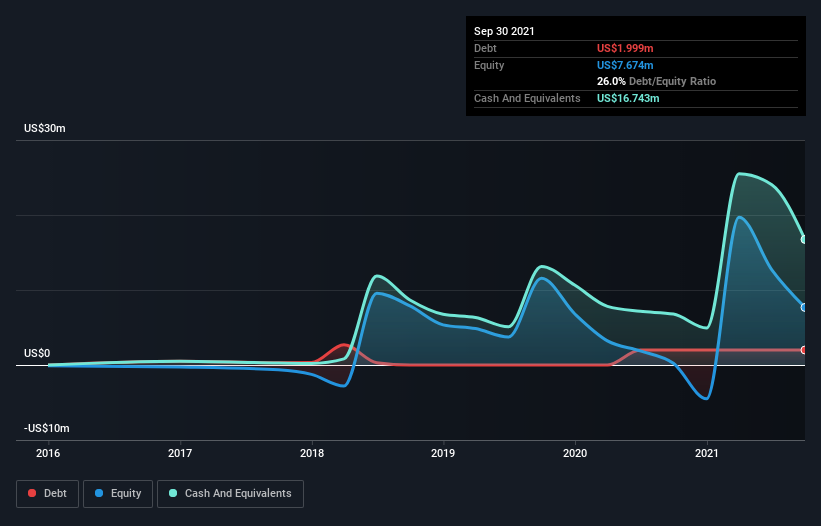

The chart below, which you can click on for greater detail, shows that HyreCar had US$2.00m in debt in September 2021; about the same as the year before. However, it does have US$16.7m in cash offsetting this, leading to net cash of US$14.7m.

A Look At HyreCar’s Liabilities

Zooming in on the latest balance sheet data, we can see that HyreCar had liabilities of US$11.9m due within 12 months and liabilities of US$2.00m due beyond that. Offsetting these obligations, it had cash of US$16.7m as well as receivables valued at US$155.5k due within 12 months. So it can boast US$2.95m more liquid assets than total liabilities.

This surplus suggests that HyreCar has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that HyreCar has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine HyreCar’s ability to maintain a healthy balance sheet going forward.

In the last year HyreCar wasn’t profitable at an EBIT level, but managed to grow its revenue by 44%, to US$33m. With any luck the company will be able to grow its way to profitability.

So How Risky Is HyreCar?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year HyreCar had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$16m of cash and made a loss of US$28m. With only US$14.7m on the balance sheet, it would appear that its going to need to raise capital again soon. With very solid revenue growth in the last year, HyreCar may be on a path to profitability. By investing before those profits, shareholders take on more risk in the hope of bigger rewards.