Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Sutro Biopharma, Inc. (NASDAQ:STRO) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

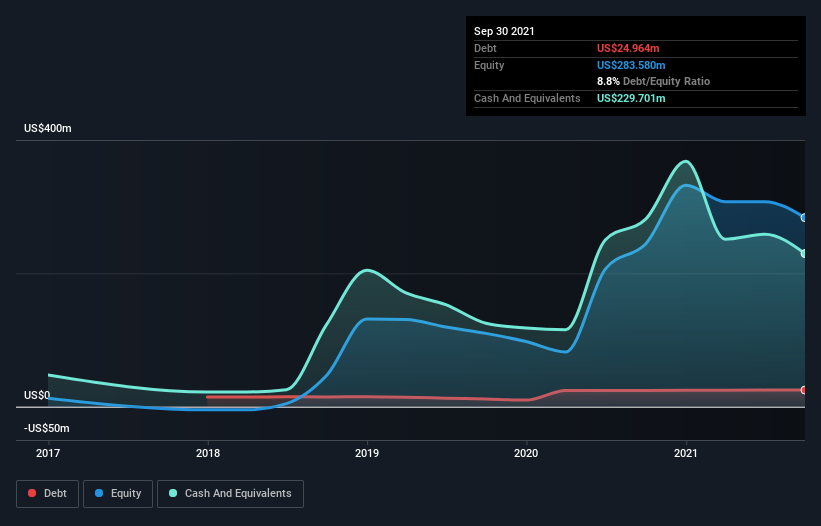

What Is Sutro Biopharma’s Net Debt?

As you can see below, Sutro Biopharma had US$25.0m of debt, at September 2021, which is about the same as the year before. You can click the chart for greater detail. But on the other hand it also has US$229.7m in cash, leading to a US$204.7m net cash position.

A Look At Sutro Biopharma’s Liabilities

The latest balance sheet data shows that Sutro Biopharma had liabilities of US$35.5m due within a year, and liabilities of US$52.4m falling due after that. Offsetting these obligations, it had cash of US$229.7m as well as receivables valued at US$12.3m due within 12 months. So it can boast US$154.1m more liquid assets than total liabilities.

This excess liquidity suggests that Sutro Biopharma is taking a careful approach to debt. Given it has easily adequate short term liquidity, we don’t think it will have any issues with its lenders. Succinctly put, Sutro Biopharma boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Sutro Biopharma’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Sutro Biopharma reported revenue of US$60m, which is a gain of 30%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is Sutro Biopharma?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Sutro Biopharma had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$93m of cash and made a loss of US$127m. But at least it has US$204.7m on the balance sheet to spend on growth, near-term. Sutro Biopharma’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. The balance sheet is clearly the area to focus on when you are analysing debt.