The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, FireEye, Inc. (NASDAQ:FEYE) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

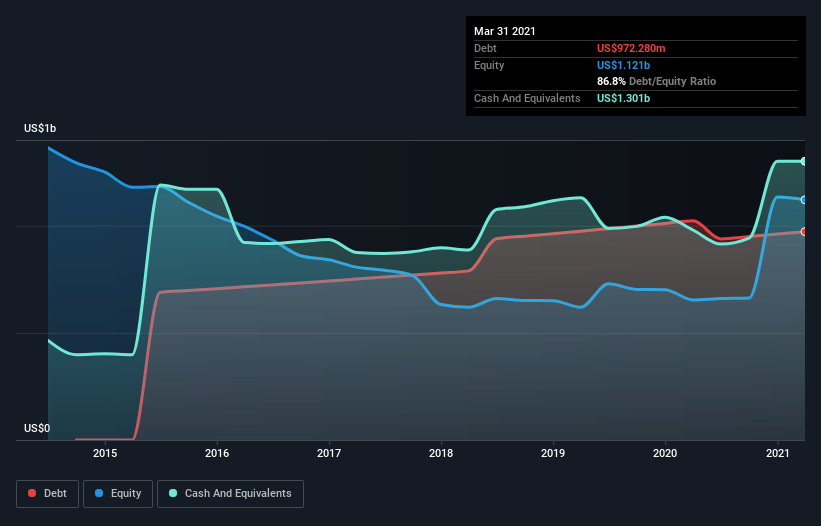

What Is FireEye’s Net Debt?

As you can see below, FireEye had US$972.3m of debt at March 2021, down from US$1.02b a year prior. But it also has US$1.30b in cash to offset that, meaning it has US$328.4m net cash.

How Healthy Is FireEye’s Balance Sheet?

The latest balance sheet data shows that FireEye had liabilities of US$710.0m due within a year, and liabilities of US$1.35b falling due after that. On the other hand, it had cash of US$1.30b and US$109.2m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$654.4m.

Given FireEye has a market capitalization of US$4.80b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, FireEye boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine FireEye’s ability to maintain a healthy balance sheet going forward.

Over 12 months, FireEye reported revenue of US$962m, which is a gain of 6.5%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is FireEye?

While FireEye lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$116m. So taking that on face value, and considering the net cash situation, we don’t think that the stock is too risky in the near term. Until we see some positive EBIT, we’re a bit cautious of the stock, not least because of the rather modest revenue growth. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.