Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Scorpio Tankers Inc. (NYSE:STNG) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

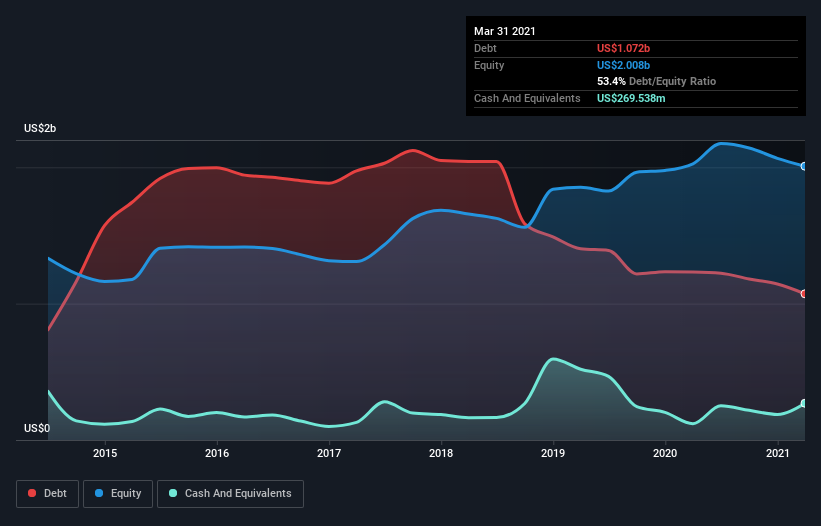

What Is Scorpio Tankers’s Debt?

As you can see below, Scorpio Tankers had US$1.07b of debt at March 2021, down from US$1.23b a year prior. However, because it has a cash reserve of US$269.5m, its net debt is less, at about US$802.6m.

A Look At Scorpio Tankers’ Liabilities

The latest balance sheet data shows that Scorpio Tankers had liabilities of US$354.4m due within a year, and liabilities of US$2.84b falling due after that. On the other hand, it had cash of US$269.5m and US$45.1m worth of receivables due within a year. So it has liabilities totalling US$2.88b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$1.26b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Scorpio Tankers would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn’t worry about Scorpio Tankers’s net debt to EBITDA ratio of 2.5, we think its super-low interest cover of 1.1 times is a sign of high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Sadly, Scorpio Tankers’s EBIT actually dropped 9.2% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Scorpio Tankers’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Scorpio Tankers actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

On the face of it, Scorpio Tankers’s interest cover left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least it’s pretty decent at converting EBIT to free cash flow; that’s encouraging. We’re quite clear that we consider Scorpio Tankers to be really rather risky, as a result of its balance sheet health. For this reason we’re pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.