Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Fastenal Company (NASDAQ:FAST) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Fastenal Carry?

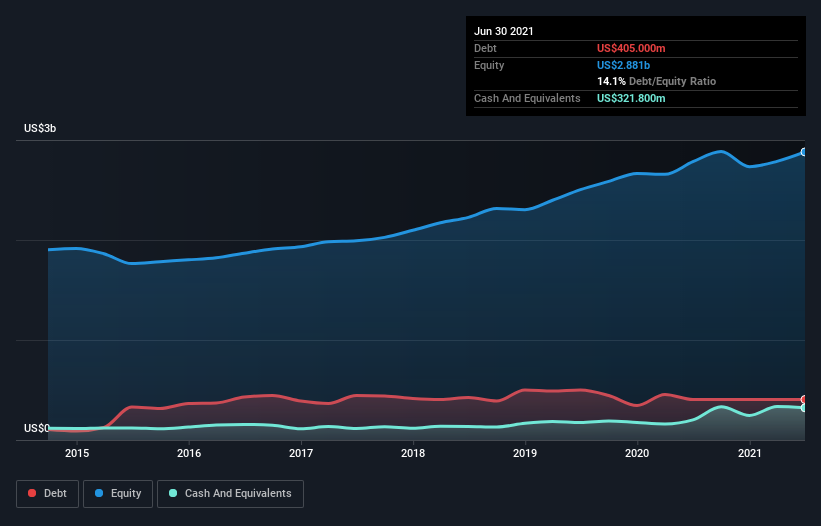

As you can see below, Fastenal had US$405.0m of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$321.8m, its net debt is less, at about US$83.2m.

How Healthy Is Fastenal’s Balance Sheet?

We can see from the most recent balance sheet that Fastenal had liabilities of US$650.2m falling due within a year, and liabilities of US$635.6m due beyond that. On the other hand, it had cash of US$321.8m and US$908.9m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$55.1m.

This state of affairs indicates that Fastenal’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$30.6b company is struggling for cash, we still think it’s worth monitoring its balance sheet. But either way, Fastenal has virtually no net debt, so it’s fair to say it does not have a heavy debt load!

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With debt at a measly 0.063 times EBITDA and EBIT covering interest a whopping 119 times, it’s clear that Fastenal is not a desperate borrower. Indeed relative to its earnings its debt load seems light as a feather. The good news is that Fastenal has increased its EBIT by 3.9% over twelve months, which should ease any concerns about debt repayment. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Fastenal’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Fastenal recorded free cash flow worth 66% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that Fastenal’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its net debt to EBITDA is also very heartening. Looking at the bigger picture, we think Fastenal’s use of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity.