Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Bilibili Inc. (NASDAQ:BILI) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Bilibili Carry?

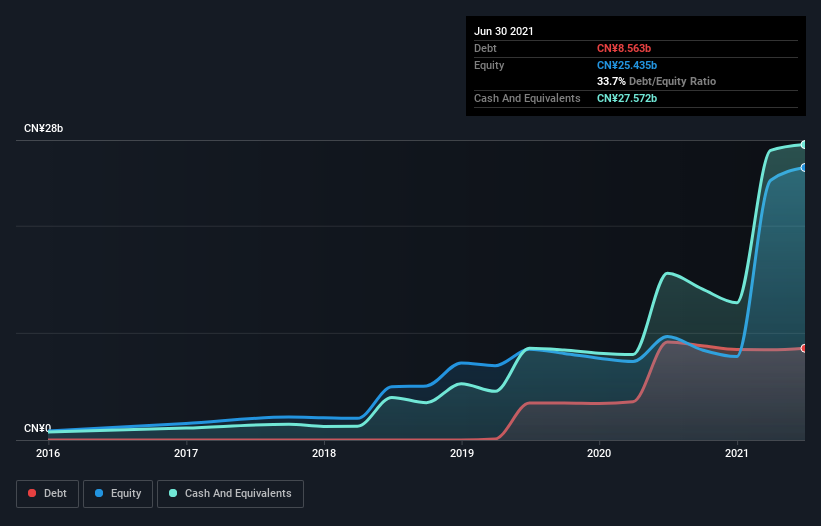

You can click the graphic below for the historical numbers, but it shows that Bilibili had CN¥8.56b of debt in June 2021, down from CN¥9.14b, one year before. But on the other hand it also has CN¥27.6b in cash, leading to a CN¥19.0b net cash position.

How Strong Is Bilibili’s Balance Sheet?

According to the last reported balance sheet, Bilibili had liabilities of CN¥9.40b due within 12 months, and liabilities of CN¥8.46b due beyond 12 months. Offsetting this, it had CN¥27.6b in cash and CN¥1.38b in receivables that were due within 12 months. So it actually has CN¥11.1b more liquid assets than total liabilities.

This short term liquidity is a sign that Bilibili could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Bilibili has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Bilibili can strengthen its balance sheet over time.

Over 12 months, Bilibili reported revenue of CN¥15b, which is a gain of 76%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is Bilibili?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Bilibili lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through CN¥1.5b of cash and made a loss of CN¥3.9b. While this does make the company a bit risky, it’s important to remember it has net cash of CN¥19.0b. That means it could keep spending at its current rate for more than two years. Bilibili’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards.