Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Dynavax Technologies Corporation (NASDAQ:DVAX) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Dynavax Technologies Carry?

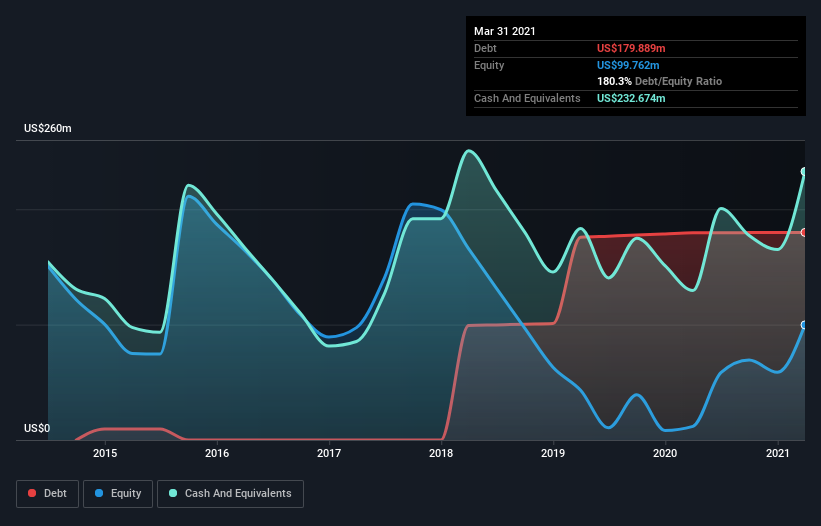

The chart below, which you can click on for greater detail, shows that Dynavax Technologies had US$179.9m in debt in March 2021; about the same as the year before. But on the other hand it also has US$232.7m in cash, leading to a US$52.8m net cash position.

A Look At Dynavax Technologies’ Liabilities

Zooming in on the latest balance sheet data, we can see that Dynavax Technologies had liabilities of US$109.4m due within 12 months and liabilities of US$280.9m due beyond that. Offsetting these obligations, it had cash of US$232.7m as well as receivables valued at US$84.0m due within 12 months. So its liabilities total US$73.7m more than the combination of its cash and short-term receivables.

Of course, Dynavax Technologies has a market capitalization of US$939.6m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Dynavax Technologies also has more cash than debt, so we’re pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Dynavax Technologies’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Dynavax Technologies reported revenue of US$119m, which is a gain of 195%, although it did not report any earnings before interest and tax. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Dynavax Technologies?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year Dynavax Technologies had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$31m of cash and made a loss of US$62m. Given it only has net cash of US$52.8m, the company may need to raise more capital if it doesn’t reach break-even soon. The good news for shareholders is that Dynavax Technologies has dazzling revenue growth, so there’s a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.