Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Greenlane Holdings, Inc. (NASDAQ:GNLN) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Greenlane Holdings’s Net Debt?

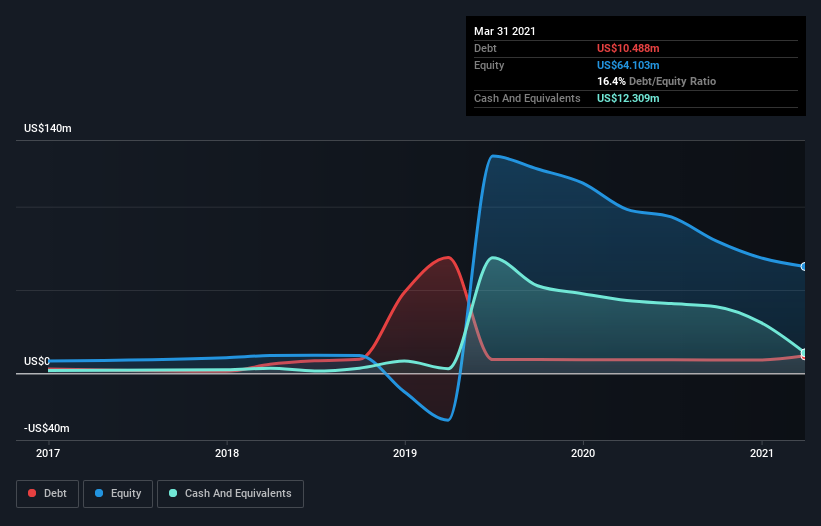

As you can see below, at the end of March 2021, Greenlane Holdings had US$10.5m of debt, up from US$8.16m a year ago. Click the image for more detail. But it also has US$12.3m in cash to offset that, meaning it has US$1.82m net cash.

A Look At Greenlane Holdings’ Liabilities

We can see from the most recent balance sheet that Greenlane Holdings had liabilities of US$31.9m falling due within a year, and liabilities of US$13.1m due beyond that. Offsetting this, it had US$12.3m in cash and US$11.5m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$21.1m.

Given Greenlane Holdings has a market capitalization of US$184.2m, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Greenlane Holdings also has more cash than debt, so we’re pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Greenlane Holdings’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Greenlane Holdings made a loss at the EBIT level, and saw its revenue drop to US$138m, which is a fall of 18%. We would much prefer see growth.

So How Risky Is Greenlane Holdings?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Greenlane Holdings lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$28m and booked a US$14m accounting loss. With only US$1.82m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, we’d say the stock is a bit risky, and we’re usually very cautious until we see positive free cash flow. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.