David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Dorian LPG Ltd. (NYSE:LPG) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is DorianG’s Debt?

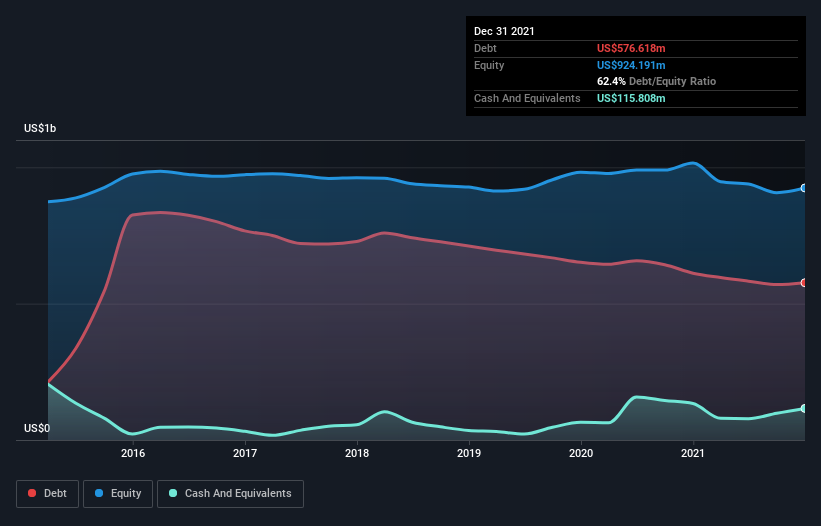

As you can see below, DorianG had US$576.6m of debt at December 2021, down from US$611.7m a year prior. However, it does have US$115.8m in cash offsetting this, leading to net debt of about US$460.8m.

A Look At DorianG’s Liabilities

The latest balance sheet data shows that DorianG had liabilities of US$94.9m due within a year, and liabilities of US$509.2m falling due after that. Offsetting this, it had US$115.8m in cash and US$47.5m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$440.8m.

This deficit is considerable relative to its market capitalization of US$507.8m, so it does suggest shareholders should keep an eye on DorianG’s use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

DorianG has a debt to EBITDA ratio of 2.8 and its EBIT covered its interest expense 5.4 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Unfortunately, DorianG’s EBIT flopped 15% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine DorianG’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, DorianG actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Neither DorianG’s ability to grow its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. Taking the abovementioned factors together we do think DorianG’s debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now.