Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Molina Healthcare, Inc. (NYSE:MOH) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Molina Healthcare’s Debt?

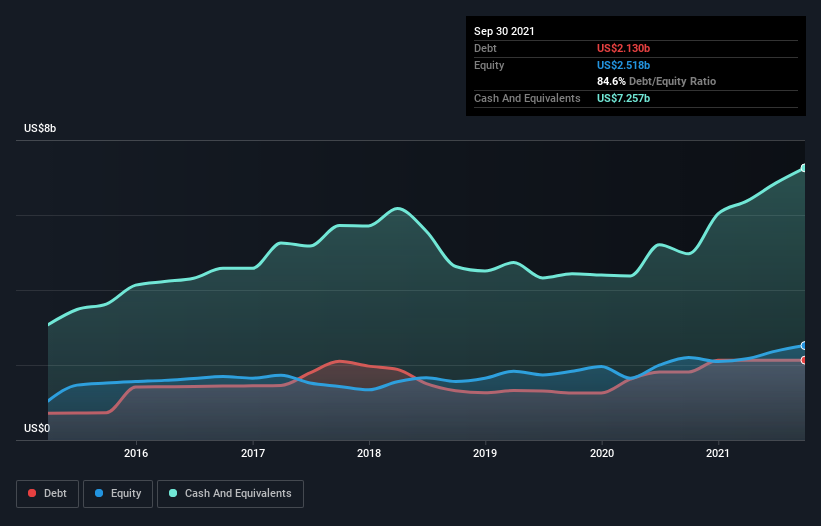

The image below, which you can click on for greater detail, shows that at September 2021 Molina Healthcare had debt of US$2.13b, up from US$1.81b in one year. But on the other hand it also has US$7.26b in cash, leading to a US$5.13b net cash position.

A Look At Molina Healthcare’s Liabilities

The latest balance sheet data shows that Molina Healthcare had liabilities of US$6.07b due within a year, and liabilities of US$2.45b falling due after that. On the other hand, it had cash of US$7.26b and US$1.91b worth of receivables due within a year. So it actually has US$654.0m more liquid assets than total liabilities.

This short term liquidity is a sign that Molina Healthcare could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Molina Healthcare has more cash than debt is arguably a good indication that it can manage its debt safely.

In fact Molina Healthcare’s saving grace is its low debt levels, because its EBIT has tanked 34% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Molina Healthcare can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Molina Healthcare may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Molina Healthcare actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Molina Healthcare has net cash of US$5.13b, as well as more liquid assets than liabilities. And it impressed us with free cash flow of US$2.7b, being 111% of its EBIT. So we are not troubled with Molina Healthcare’s debt use. There’s no doubt that we learn most about debt from the balance sheet.