The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Cloudflare, Inc. (NYSE:NET) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Cloudflare’s Debt?

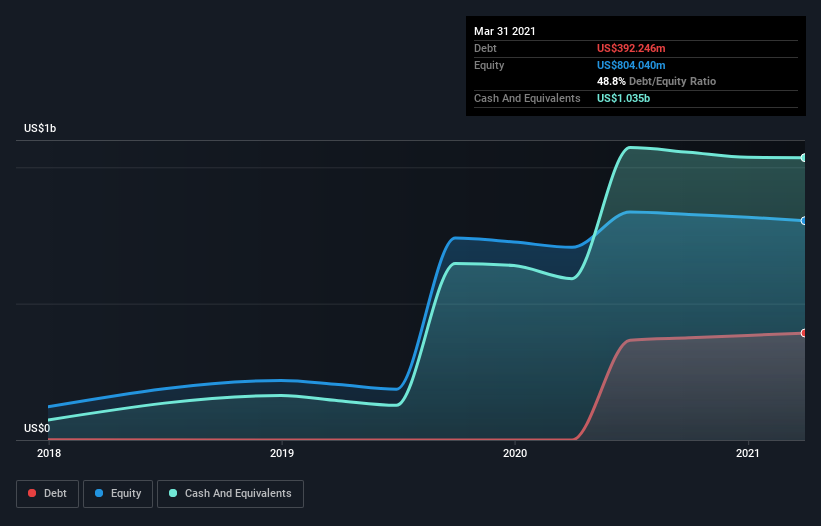

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Cloudflare had US$392.2m of debt, an increase on none, over one year. However, it does have US$1.04b in cash offsetting this, leading to net cash of US$643.0m.

How Healthy Is Cloudflare’s Balance Sheet?

According to the last reported balance sheet, Cloudflare had liabilities of US$168.1m due within 12 months, and liabilities of US$433.3m due beyond 12 months. Offsetting this, it had US$1.04b in cash and US$74.9m in receivables that were due within 12 months. So it actually has US$508.6m more liquid assets than total liabilities.

This state of affairs indicates that Cloudflare’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$36.3b company is struggling for cash, we still think it’s worth monitoring its balance sheet. Succinctly put, Cloudflare boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Cloudflare can strengthen its balance sheet over time.

In the last year Cloudflare wasn’t profitable at an EBIT level, but managed to grow its revenue by 51%, to US$478m. With any luck the company will be able to grow its way to profitability.

So How Risky Is Cloudflare?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Cloudflare had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$64m of cash and made a loss of US$127m. But the saving grace is the US$643.0m on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. With very solid revenue growth in the last year, Cloudflare may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start.