Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that CyberArk Software Ltd. (NASDAQ:CYBR) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does CyberArk Software Carry?

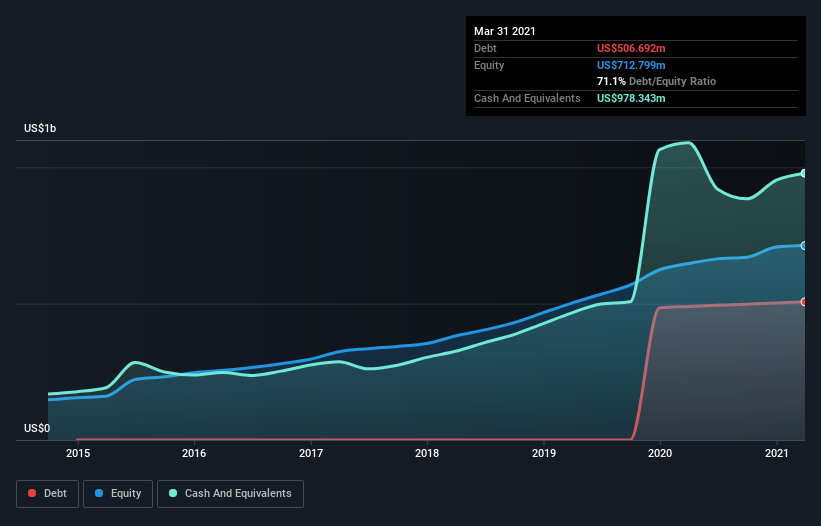

As you can see below, CyberArk Software had US$483.5m of debt, at March 2021, which is about the same as the year before. You can click the chart for greater detail. But it also has US$978.3m in cash to offset that, meaning it has US$494.9m net cash.

How Healthy Is CyberArk Software’s Balance Sheet?

The latest balance sheet data shows that CyberArk Software had liabilities of US$245.8m due within a year, and liabilities of US$613.6m falling due after that. Offsetting these obligations, it had cash of US$978.3m as well as receivables valued at US$66.7m due within 12 months. So it actually has US$185.7m more liquid assets than total liabilities.

This short term liquidity is a sign that CyberArk Software could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, CyberArk Software boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine CyberArk Software’s ability to maintain a healthy balance sheet going forward.

In the last year CyberArk Software wasn’t profitable at an EBIT level, but managed to grow its revenue by 5.8%, to US$470m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is CyberArk Software?

While CyberArk Software lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$98m. So taking that on face value, and considering the net cash situation, we don’t think that the stock is too risky in the near term. With mediocre revenue growth in the last year, we’re don’t find the investment opportunity particularly compelling. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.