The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Cintas Corporation (NASDAQ:CTAS) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Cintas Carry?

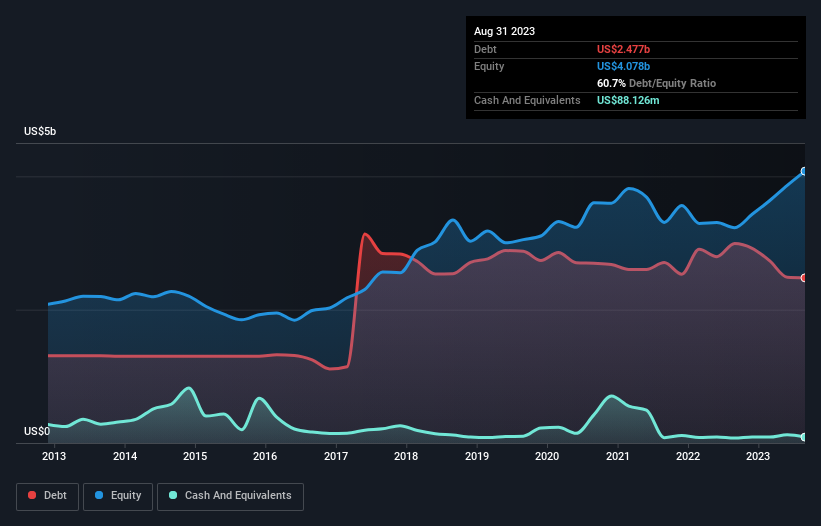

The image below, which you can click on for greater detail, shows that Cintas had debt of US$2.48b at the end of August 2023, a reduction from US$2.99b over a year. However, because it has a cash reserve of US$88.1m, its net debt is less, at about US$2.39b.

How Strong Is Cintas’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Cintas had liabilities of US$1.17b due within 12 months and liabilities of US$3.47b due beyond that. On the other hand, it had cash of US$88.1m and US$1.20b worth of receivables due within a year. So its liabilities total US$3.36b more than the combination of its cash and short-term receivables.

Since publicly traded Cintas shares are worth a very impressive total of US$52.8b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Cintas’s net debt is only 1.1 times its EBITDA. And its EBIT easily covers its interest expense, being 17.6 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. And we also note warmly that Cintas grew its EBIT by 14% last year, making its debt load easier to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Cintas can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Cintas recorded free cash flow worth 76% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that Cintas’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Zooming out, Cintas seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. When analysing debt levels, the balance sheet is the obvious place to start.