Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Arcimoto, Inc. (NASDAQ:FUV) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

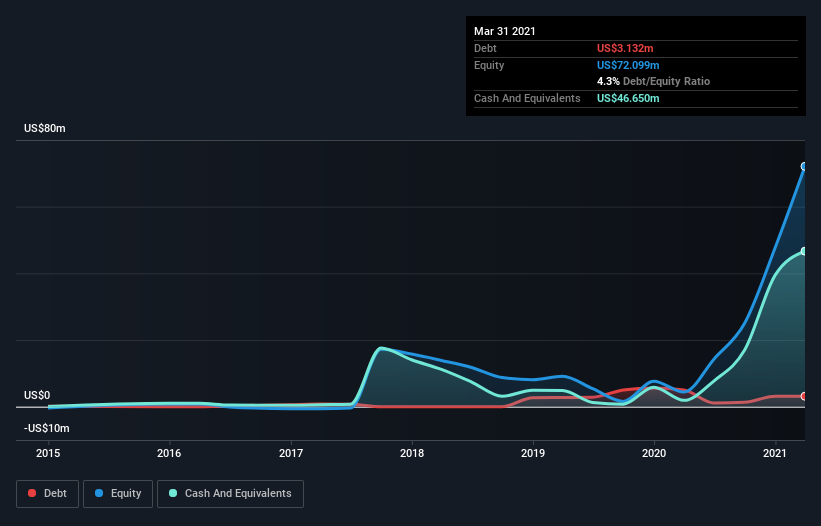

How Much Debt Does Arcimoto Carry?

As you can see below, Arcimoto had US$3.13m of debt at March 2021, down from US$5.01m a year prior. However, its balance sheet shows it holds US$46.7m in cash, so it actually has US$43.5m net cash.

How Healthy Is Arcimoto’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Arcimoto had liabilities of US$3.47m due within 12 months and liabilities of US$3.09m due beyond that. Offsetting these obligations, it had cash of US$46.7m as well as receivables valued at US$13.9k due within 12 months. So it can boast US$40.1m more liquid assets than total liabilities.

This surplus suggests that Arcimoto has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Arcimoto boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Arcimoto’s ability to maintain a healthy balance sheet going forward.

In the last year Arcimoto wasn’t profitable at an EBIT level, but managed to grow its revenue by 84%, to US$3.0m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Arcimoto?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Arcimoto had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$22m of cash and made a loss of US$19m. Given it only has net cash of US$43.5m, the company may need to raise more capital if it doesn’t reach break-even soon. With very solid revenue growth in the last year, Arcimoto may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.