The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Splunk Inc. (NASDAQ:SPLK) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Splunk Carry?

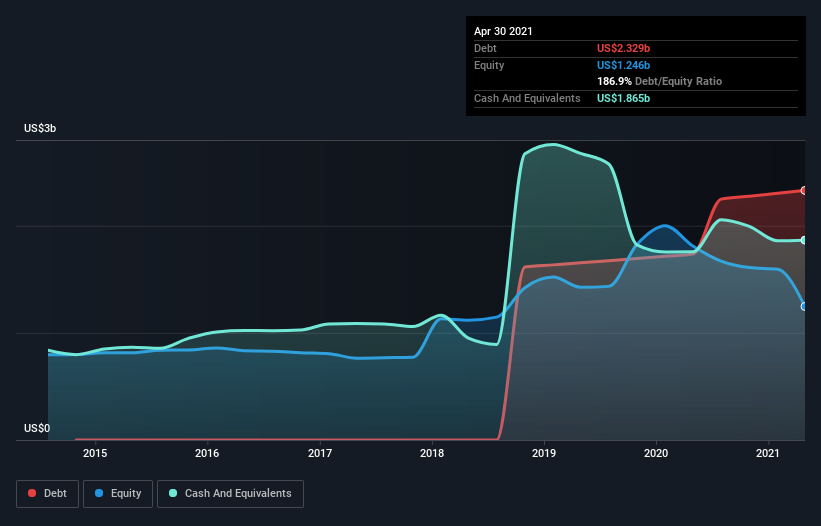

The image below, which you can click on for greater detail, shows that at April 2021 Splunk had debt of US$2.27b, up from US$1.74b in one year. However, it also had US$1.87b in cash, and so its net debt is US$399.7m.

How Healthy Is Splunk’s Balance Sheet?

The latest balance sheet data shows that Splunk had liabilities of US$1.40b due within a year, and liabilities of US$2.65b falling due after that. Offsetting this, it had US$1.87b in cash and US$775.9m in receivables that were due within 12 months. So it has liabilities totalling US$1.41b more than its cash and near-term receivables, combined.

Since publicly traded Splunk shares are worth a very impressive total of US$21.2b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Splunk’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Splunk made a loss at the EBIT level, and saw its revenue drop to US$2.3b, which is a fall of 3.0%. That’s not what we would hope to see.

Caveat Emptor

Over the last twelve months Splunk produced an earnings before interest and tax (EBIT) loss. To be specific the EBIT loss came in at US$861m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn’t help that it burned through US$204m of cash over the last year. So suffice it to say we do consider the stock to be risky.