Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that The Hain Celestial Group, Inc. (NASDAQ:HAIN) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

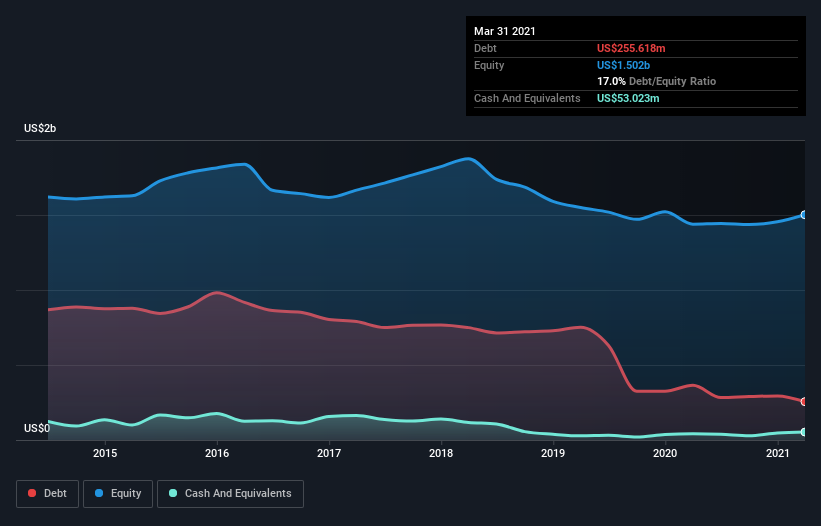

What Is Hain Celestial Group’s Debt?

As you can see below, Hain Celestial Group had US$255.6m of debt at March 2021, down from US$364.9m a year prior. However, it also had US$53.0m in cash, and so its net debt is US$202.6m.

A Look At Hain Celestial Group’s Liabilities

According to the last reported balance sheet, Hain Celestial Group had liabilities of US$331.4m due within 12 months, and liabilities of US$406.8m due beyond 12 months. Offsetting this, it had US$53.0m in cash and US$190.7m in receivables that were due within 12 months. So its liabilities total US$494.4m more than the combination of its cash and short-term receivables.

Given Hain Celestial Group has a market capitalization of US$4.02b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Hain Celestial Group’s net debt is only 0.85 times its EBITDA. And its EBIT easily covers its interest expense, being 25.9 times the size. So we’re pretty relaxed about its super-conservative use of debt. In addition to that, we’re happy to report that Hain Celestial Group has boosted its EBIT by 69%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Hain Celestial Group’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Hain Celestial Group’s free cash flow amounted to 45% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

The good news is that Hain Celestial Group’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its EBIT growth rate also supports that impression! Zooming out, Hain Celestial Group seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.