Summary

- IIPR Oct 2021 option contracts are only pricing in 9% to 11% share moves, but shares will likely move 20% or more if capital deployment falls short or exceeds expectations.

- Size of recent debt raise suggests management is confident they have a sufficient pipeline of investment to cover incremental annual interest expense of $16.5 million or $0.63 per share.

- At 11% to 12% leasing rates, IIPR will need to deploy about 50% of the $293.4 million of proceeds before $300 million debt offering is cash flow accretive.

- IIPR’s speed of capital deployment provides trading opportunities as shares could easily sink or rally 20% depending upon how the $293.4 million of proceeds are invested.

- IIPR tenant Green Thumb Industries securing $217 million of debt at 7% sends a signal to peer MSOs and is a forewarning for IIPR’s double-digit underwriting rates.

Overview of recommendation

Innovative Industrial Properties (IIPR) is a REIT that offers long-term secured financing for cannabis operators via sale leaseback structures. IIPR recently raised $300 million in debt, the interest expense of which will be a drag to cash flows of $16.5 million or $.63 per share. How the debt proceeds are deployed over the coming 6 months will provide possible catalyst for both long and short positions.

Bulls and bears alike will be looking for answers to the following as capital is deployed. Is the entire $293.4 million contracted to market leaders and well capitalized multi-state operators – MSOs – in limited-licensed states by the end of June? Or does the deployment of capital drag out for months and the tenants signed are not well capitalized MSOs, like Green Thumb Industries (OTCQX:GTBIF), but instead lower credit quality tenants in highly competitive markets?

For traders, the pace and scale of capital deployment could offer great trades on both the long and short side. Shares could easily sink or rip 20% depending upon how the $293.4 million is deployed, but October 2021 options contracts, as of this writing, are only pricing in moves of 9% to 11%.

Shares will react favorably if (NYSE:IIPR) signs big dollar deals with respected and well capitalized MSOs in limited license states like Massachusetts or Illinois. The sooner the capital is deployed, the more potential for the shares to rally. And if there’s a heavy short interest in the shares, you could see far more than a 20% move to the upside.

On the other hand, if by end of June IIPR only has $50 million locked up into highly competitive markets like California, Oregon or Colorado, investors could get spooked and the shares could sell off. As of this writing, IIPR has announced a total of $18.1 million in new investment subsequent to the debt raise. Come this October if the entire $293.4 million has not been invested, investors will be asking a lot of questions as to the timing and size of the debt deal and the shares will likely sell off more than 20%.

For long term “buy and hold” investors, I reiterate my March 23 recommendation that, notwithstanding near term trading opportunities, investors understand the risk to the business model in a post-prohibition world and consider hedging or selling position. The entire $293.4 million could be contracted as of this writing, and my recommendation would not change. In a post-prohibition world, underwriting margins will contract materially, and IIPR’s real estate is at risk of obsolescence if cannabis can be imported from Mexico and Latin America where cultivation cost is 90% lower.

For short investors, consider hedging position with calls. IIPR wouldn’t be raising $300 million in debt unless they were confident in closing at least $100 million in deals fairly quickly to cover the additional interest expense.

Since my first warning on IIPR last December IIPR, shares are up 14% versus the S&P 500 up 14.5%. Since my second warning on IIPR last March, IIPR shares are up 4.5% versus the S&P 500 up 7.5%. IIPR’s marginal underperformance relative to the S&P 500 over the past month may suggest greater investor awareness on risks to IIPR in a post-prohibition world.

IIPR needs to invest $100 to $150 million to cover additional interest expense from $300 million debt raise

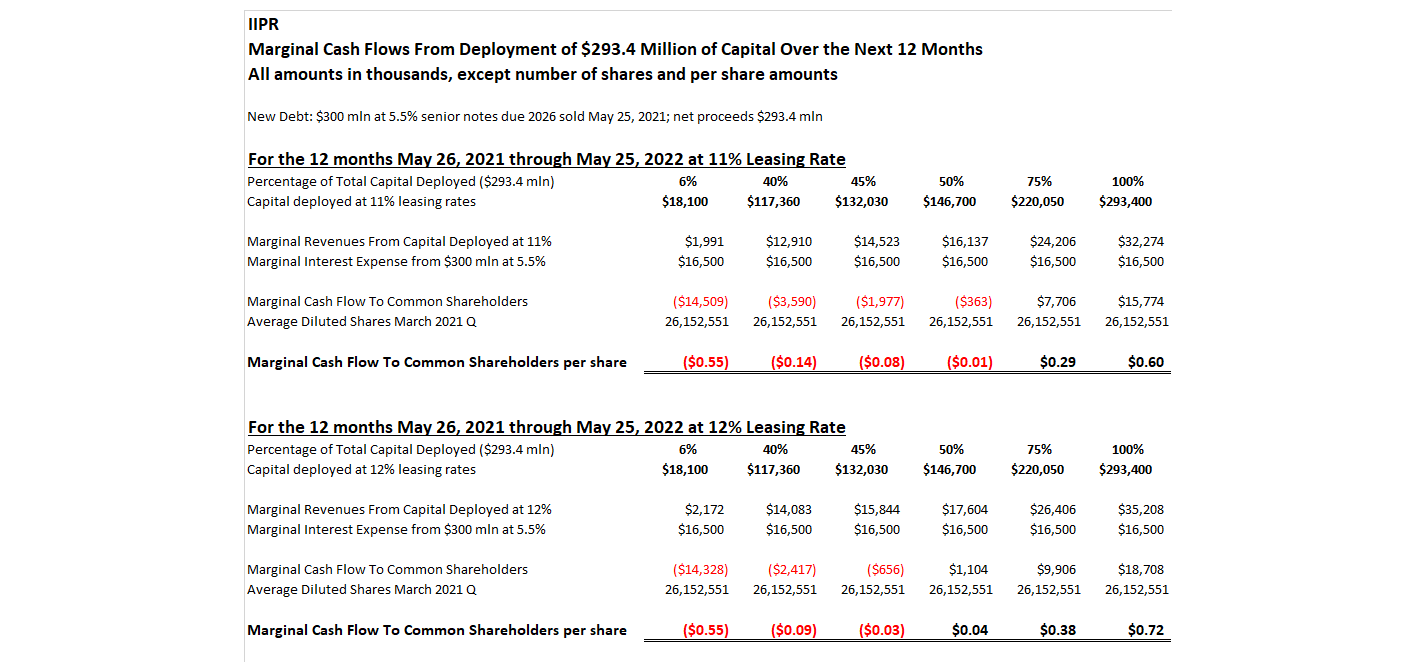

On May 25, 2021, IIPR raised net proceeds of $293.4 million from a $300 million 5-year senior note offering priced at 5.5%. To cover the annual interest expense of $16.5 million, IIPR will need to deploy capital of $100 million at 16.5% or $120 million at 13.75% or $150 million at 11%, etc. Before any of the proceeds are invested, IIPR’s $300 million debt offering is a drag on cash flow to common shareholders by $.63 per share. With the May 27 announced deal of $18.1 million with Temescal Wellness, the dilutive impact of the debt offering as of this writing is $.55 per share. See the math in the chart below for the dilutive and accretive impact from deployment of the loan proceeds.

The chart above illustrates that with 11% to 12% leasing rates, IIPR will need to deploy about 50% of the $293.4 million in capital before the $300 million debt offering is cash flow accretive to common shareholders. As illustrated, when the full net proceeds of $293.4 million have been deployed, then the $300 million in debt raised will be $.60 per share cash flow accretive at 11% leasing rate and $.72 per share cash flow accretive at 12% leasing rate.

With the May 27 Temescal Wellness deal of $18.1 million, only 6% of the $293.4 million of net debt proceeds has been deployed leaving the $300 million debt raise a $.55 per share hit to cash flows as illustrated in the chart above.

Clearly, IIPR management understands this math and wouldn’t take on an annual interest burden of $16.5 million without having some confidence they could deploy sufficient capital at double-digit rates to at a very minimum cover the additional interest cost on the $300 million of new debt. Accordingly, look for IIPR to announce deals aggregating $100 to $150 million to offset the additional interest expense.

Odds are IIPR announces over $200 million of new investment before September 30, 2021

The speed of capital deployment should be frontal lobe for investors. Remember, the $100 to $150 million of new investment is just to cover the additional interest cost from the $300 million debt raise. To be materially accretive to cash flow, IIPR will need to deploy more than $200 million at double-digit rates. So, don’t be surprised if IIPR announces deals worth well over $200 million before September 30, 2021. Again, IIPR has gone through this math, so odds are they feel confident in their deal pipeline.

On the other hand, investors will likely get spooked if by late August IIPR has not announced deals around $100 million. If by this September IIPR has not announced deals exceeding $100 million, investors will be asking questions as to the size and timing of the $300 million debt raise. Why the rush to raise $300 million in debt if there was no solid pipeline to invest the proceeds timely? Has something changed from when IIPR first contemplated the debt raise? Is there concern the cost of the debt would be higher later in the year?

The indenture of the $300 million note includes a provision the interest rate on the notes will increase to a range of 6% to 6.5% in the event of a credit downgrade. Per IIPR’s May 25, 2021 8-K

Pursuant to the terms of the indenture, if the debt rating on the notes is downgraded or withdrawn entirely, interest on the notes will increase to a range of 6.0% to 6.5% based on such debt rating.

If IIPR’s tenants were to default, IIPR’s credit standing under the notes could change and IIPR’s annual interest expense could increase from $16.5 million or $.63 per share to $19.5 million or $.75 per share.

Green Thumb Industries 7% debt financing is a forewarning for IIPR

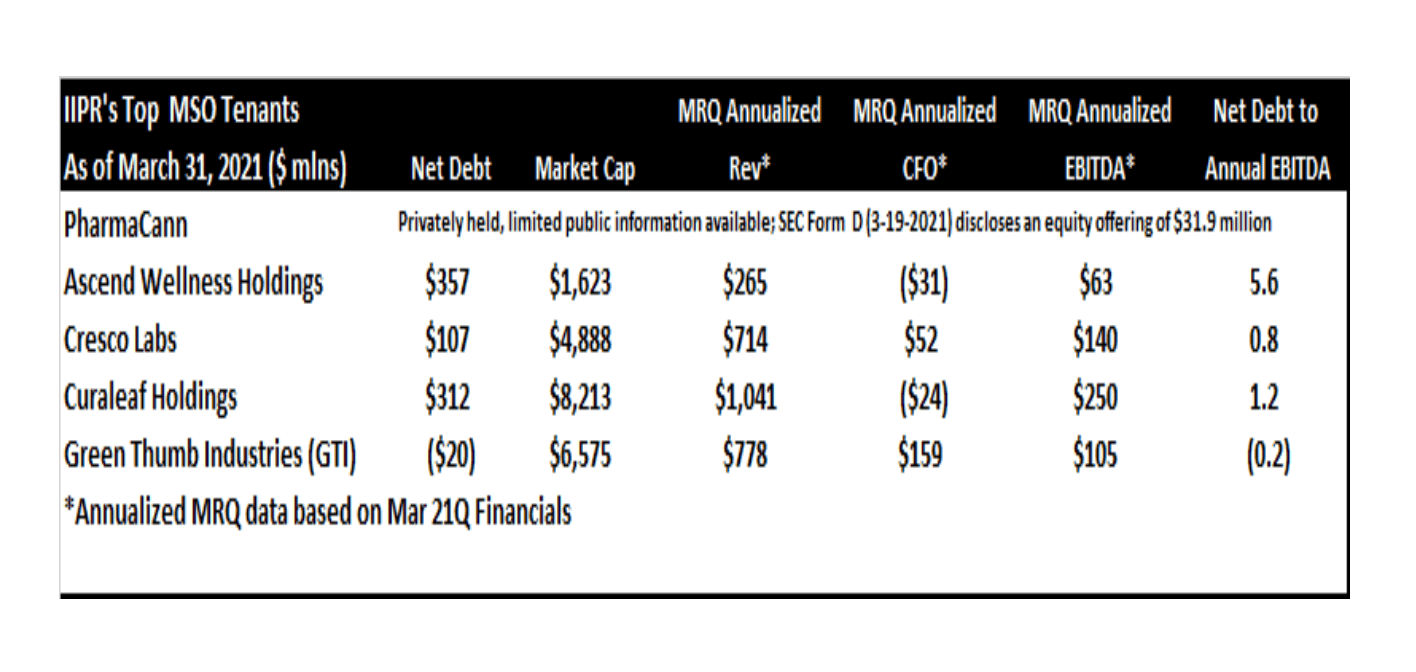

As disclosed in IIPR’s March 2021 10-Q, Green Thumb Industries has 3 leases that represented 7% of IIPR’s March 2021 quarter revenues. These 3 leases were disclosed in the December 2020 10-K, so Green Thumb Industries, arguably one of the few premier MSOs, has declined to sign any more deals with IIPR to fund their market expansion.

During the September 2020 earnings conference call last November, Green Thumb Industries CEO Ben Kovler, not only called out for banking reform to lower the cost of capital, but he specifically claimed the business was not profitable at 12% cost of capital.

So, what’s really interesting about banking change, the cost of capital and thinking about our debt, and what that cost of debt might be for the risk profile of the business that’s not profitable at 12%.

That Green Thumb Industries is telling investors 12% cost of capital hinders their profitability strikes to the core of IIPR’s business model based upon underwriting deals at rates above 11%. If 12% cost of capital hinders the profitability of one of the largest and strongest MSOs in the country, then how are smaller less capitalized cannabis operators suppose to survive paying 12%?

During the December 2020 earnings conference call last March, Ben Kovler reiterated he was not interested in another sale leaseback paying double-digit rates.

If the cost of capital goes from where it was in the rearview mirror, which was a double-digit rate with warrants or these sale leasebacks at double-digit rates, where it’s going to be very soon, which is single digit, where the credit is probably investment grade and yet we have to pay more but it’s still single digit, and then it’s going to go even lower.

Green Thumb Industries eschewed IIPR in their most recent capital raise and instead announced they had secured $217 million of senior debt priced at 7% with 1.459 million 5-year warrants with an exercise price of $32.68 per share.

That Green Thumb Industries was able to secure single-digit financing even before any banking reform has two critical negative implications for IIPR.

First, it signals to competitor MSOs like Cresco Labs (OTCQX:CRLBF) and Trulieve Cannabis (TCNNF) that single-digit cost of debt is available even before banking reform. To compete with Green Thumb Industries and to present themselves as best in class peers, competing MSOs will follow Green Thumb Industries and avoid double-digit costs of capital like IIPR’s sale leaseback offering. If Green Thumb Industries is able to secure over $200 million at 7%, then what does it say about Cresco Labs, Ascend Wellness Holdings (OTCPK:AWWH), Curaleaf (OTCPK:CURLF), Trulieve, etc, if they have no choice but to rely upon IIPR’s double-digit sale leasebacks for capital?

Second, Green Thumb Industries securing debt at nearly half the cost IIPR charges is a forewarning on where underwriting spreads are going for investment grade cannabis operators. If IIPR wants to keep their underwriting rates at low-teens with annual escalators driving rates to over 20%, then they’ll need to target lower credit quality tenants to grow their investment portfolio as investment grade tenants will demand single-digit rates.

As illustrated in the chart above, it appears losing Green Thumb Industries (7% of IIPR revenues) for new deals is a major blow for IIPR’s overall portfolio credit quality going forward. Green Thumb Industries appears to be the most credit worthy of IIPR’s top 5 tenants. Ascend Wellness Holdings, levered 5.6x and representing 10% of IIPR’s March 2021 revenues, recently filed to sell 10 million common shares, which should ameliorate their high leverage. No public information is available to assess the credit quality of IIPR’s top tenant, PharmaCann who contributed 13% to March 2021 revenues.

Conclusion

So the clock is ticking and IIPR will need to thread the needle of securing double-digit lease rates while also signing tenants that will survive in a post-prohibition world. There is no shortage of cash burning cannabis operators on the verge of insolvency, so IIPR will have no problem finding willing tenants amenable to signing up for double-digit financing rates. The challenge for IIPR is finding those who will remain viable entities for the duration of their 16-year lease. With larger and better capitalized MSOs like Green Thumb Industries securing capital at single-digit rates, how will IIPR’s smaller less capitalized tenants survive?