The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Slack Technologies, Inc. (NYSE:WORK) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Slack Technologies’s Net Debt?

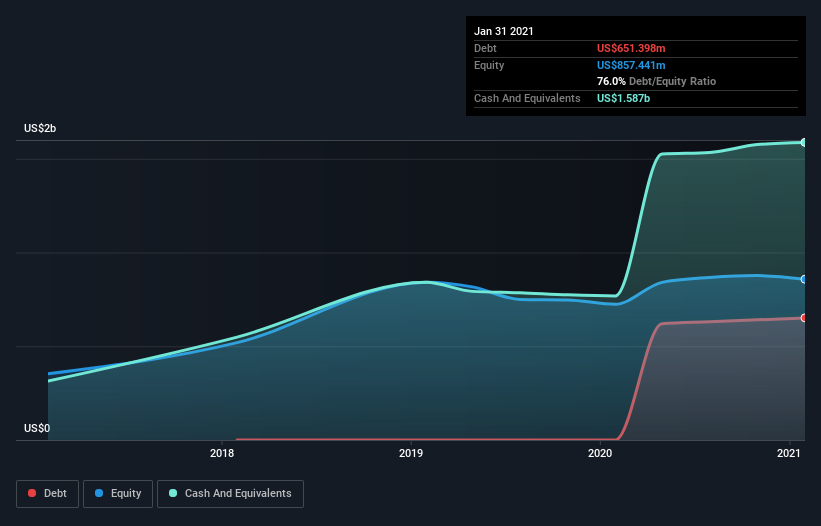

The image below, which you can click on for greater detail, shows that at January 2021 Slack Technologies had debt of US$651.4m, up from none in one year. But on the other hand it also has US$1.59b in cash, leading to a US$935.9m net cash position.

A Look At Slack Technologies’ Liabilities

The latest balance sheet data shows that Slack Technologies had liabilities of US$697.1m due within a year, and liabilities of US$879.1m falling due after that. Offsetting this, it had US$1.59b in cash and US$237.4m in receivables that were due within 12 months. So it can boast US$248.4m more liquid assets than total liabilities.

This state of affairs indicates that Slack Technologies’ balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$25.5b company is struggling for cash, we still think it’s worth monitoring its balance sheet. Simply put, the fact that Slack Technologies has more cash than debt is arguably a good indication that it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Slack Technologies’s ability to maintain a healthy balance sheet going forward.

In the last year Slack Technologies wasn’t profitable at an EBIT level, but managed to grow its revenue by 43%, to US$903m. With any luck the company will be able to grow its way to profitability.

So How Risky Is Slack Technologies?

While Slack Technologies lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$60m. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. We think its revenue growth of 43% is a good sign. We’d see further strong growth as an optimistic indication. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.