Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Avnet, Inc. (NASDAQ:AVT) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Avnet’s Net Debt?

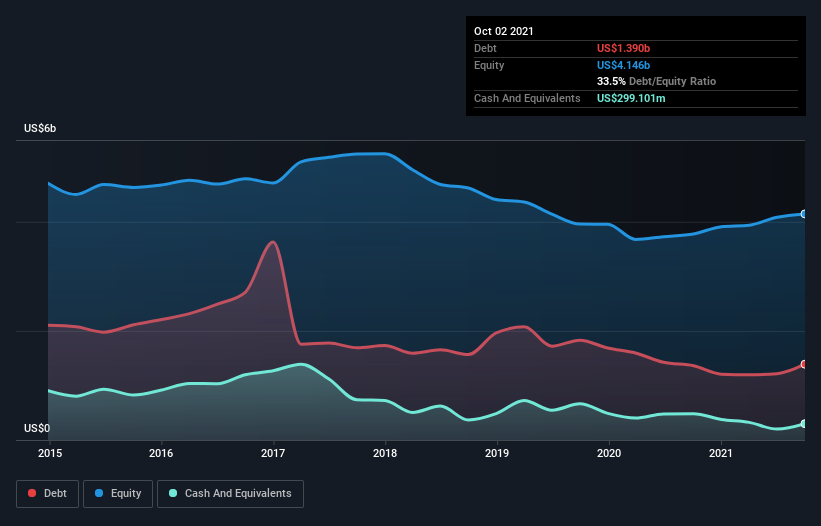

The chart below, which you can click on for greater detail, shows that Avnet had US$1.39b in debt in October 2021; about the same as the year before. On the flip side, it has US$299.1m in cash leading to net debt of about US$1.09b.

How Healthy Is Avnet’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Avnet had liabilities of US$3.11b due within 12 months and liabilities of US$1.95b due beyond that. Offsetting this, it had US$299.1m in cash and US$3.72b in receivables that were due within 12 months. So its liabilities total US$1.05b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Avnet is worth US$3.87b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Avnet has net debt worth 1.7 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 5.6 times the interest expense. While these numbers do not alarm us, it’s worth noting that the cost of the company’s debt is having a real impact. Pleasingly, Avnet is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 166% gain in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Avnet’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Avnet actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Avnet’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Zooming out, Avnet seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. When analysing debt levels, the balance sheet is the obvious place to start.