Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies DICK’S Sporting Goods, Inc. (NYSE:DKS) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is DICK’S Sporting Goods’s Net Debt?

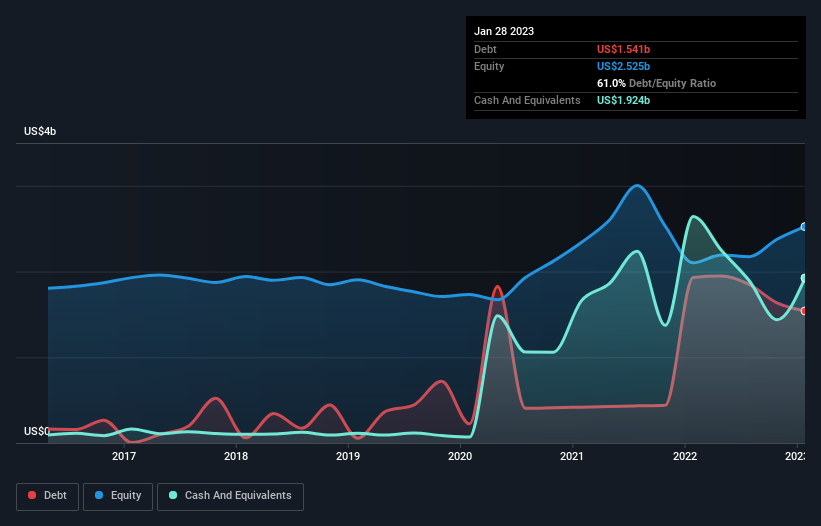

The image below, which you can click on for greater detail, shows that DICK’S Sporting Goods had debt of US$1.54b at the end of January 2023, a reduction from US$1.93b over a year. However, its balance sheet shows it holds US$1.92b in cash, so it actually has US$383.8m net cash.

A Look At DICK’S Sporting Goods’ Liabilities

The latest balance sheet data shows that DICK’S Sporting Goods had liabilities of US$2.64b due within a year, and liabilities of US$3.83b falling due after that. On the other hand, it had cash of US$1.92b and US$79.5m worth of receivables due within a year. So its liabilities total US$4.46b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because DICK’S Sporting Goods is worth a massive US$11.8b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. Despite its noteworthy liabilities, DICK’S Sporting Goods boasts net cash, so it’s fair to say it does not have a heavy debt load!

The modesty of its debt load may become crucial for DICK’S Sporting Goods if management cannot prevent a repeat of the 27% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine DICK’S Sporting Goods’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. DICK’S Sporting Goods may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, DICK’S Sporting Goods recorded free cash flow worth 75% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

Although DICK’S Sporting Goods’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$383.8m. The cherry on top was that in converted 75% of that EBIT to free cash flow, bringing in US$558m. So we are not troubled with DICK’S Sporting Goods’s debt use. When analysing debt levels, the balance sheet is the obvious place to start.