The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that CSW Industrials, Inc. (NASDAQ:CSWI) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

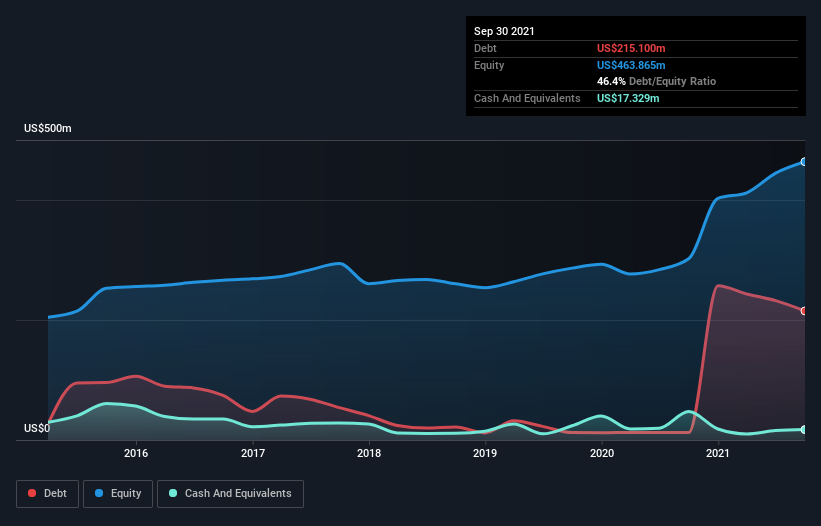

What Is CSW Industrials’s Net Debt?

As you can see below, at the end of September 2021, CSW Industrials had US$215.1m of debt, up from US$12.4m a year ago. Click the image for more detail. On the flip side, it has US$17.3m in cash leading to net debt of about US$197.8m.

How Strong Is CSW Industrials’ Balance Sheet?

According to the last reported balance sheet, CSW Industrials had liabilities of US$85.7m due within 12 months, and liabilities of US$353.4m due beyond 12 months. Offsetting these obligations, it had cash of US$17.3m as well as receivables valued at US$107.7m due within 12 months. So its liabilities total US$314.2m more than the combination of its cash and short-term receivables.

Given CSW Industrials has a market capitalization of US$1.80b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

CSW Industrials’s net debt to EBITDA ratio of about 1.6 suggests only moderate use of debt. And its strong interest cover of 18.4 times, makes us even more comfortable. In addition to that, we’re happy to report that CSW Industrials has boosted its EBIT by 33%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine CSW Industrials’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, CSW Industrials recorded free cash flow worth a fulsome 87% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Our View

CSW Industrials’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Overall, we don’t think CSW Industrials is taking any bad risks, as its debt load seems modest. So the balance sheet looks pretty healthy, to us.