David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Atmos Energy Corporation (NYSE:ATO) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Atmos Energy’s Debt?

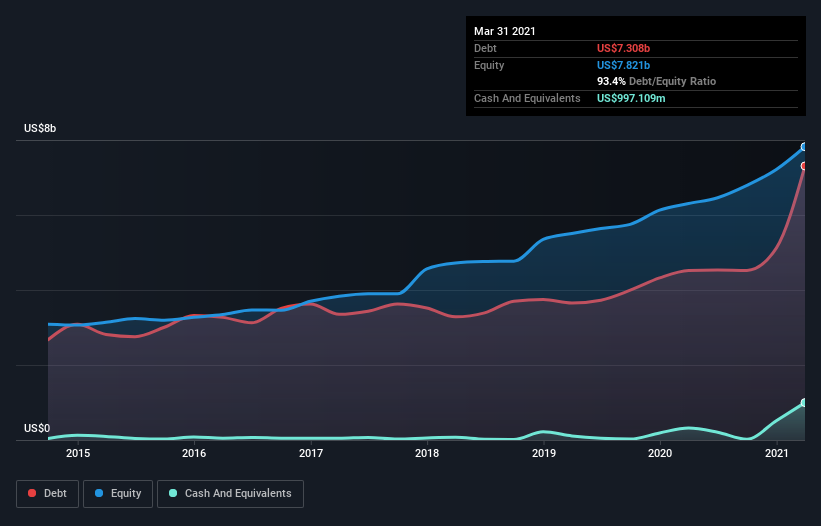

The image below, which you can click on for greater detail, shows that at March 2021 Atmos Energy had debt of US$7.31b, up from US$4.52b in one year. However, it also had US$997.1m in cash, and so its net debt is US$6.31b.

How Strong Is Atmos Energy’s Balance Sheet?

According to the last reported balance sheet, Atmos Energy had liabilities of US$871.3m due within 12 months, and liabilities of US$10.7b due beyond 12 months. On the other hand, it had cash of US$997.1m and US$469.6m worth of receivables due within a year. So it has liabilities totalling US$10.1b more than its cash and near-term receivables, combined.

This is a mountain of leverage even relative to its gargantuan market capitalization of US$13.2b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Atmos Energy has a debt to EBITDA ratio of 4.6, which signals significant debt, but is still pretty reasonable for most types of business. However, its interest coverage of 11.4 is very high, suggesting that the interest expense on the debt is currently quite low. One way Atmos Energy could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 16%, as it did over the last year. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Atmos Energy’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Atmos Energy saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Atmos Energy’s conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example its interest cover was refreshing. We should also note that Gas Utilities industry companies like Atmos Energy commonly do use debt without problems. Taking the abovementioned factors together we do think Atmos Energy’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.