David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Adecoagro S.A. (NYSE:AGRO) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Adecoagro’s Debt?

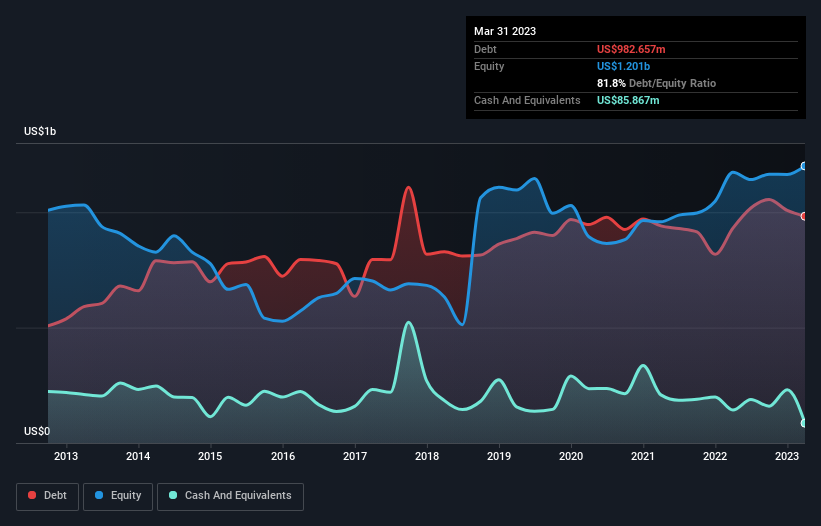

You can click the graphic below for the historical numbers, but it shows that as of March 2023 Adecoagro had US$982.7m of debt, an increase on US$930.9m, over one year. On the flip side, it has US$85.9m in cash leading to net debt of about US$896.8m.

How Strong Is Adecoagro’s Balance Sheet?

The latest balance sheet data shows that Adecoagro had liabilities of US$494.9m due within a year, and liabilities of US$1.37b falling due after that. On the other hand, it had cash of US$85.9m and US$137.1m worth of receivables due within a year. So its liabilities total US$1.64b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$1.09b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Adecoagro would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Adecoagro has net debt worth 2.2 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 3.0 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. Unfortunately, Adecoagro’s EBIT flopped 16% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Adecoagro’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Adecoagro’s free cash flow amounted to 36% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

To be frank both Adecoagro’s EBIT growth rate and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. Having said that, its ability handle its debt, based on its EBITDA, isn’t such a worry. Taking into account all the aforementioned factors, it looks like Adecoagro has too much debt. While some investors love that sort of risky play, it’s certainly not our cup of tea. There’s no doubt that we learn most about debt from the balance sheet.