David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies ACCO Brands Corporation (NYSE:ACCO) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does ACCO Brands Carry?

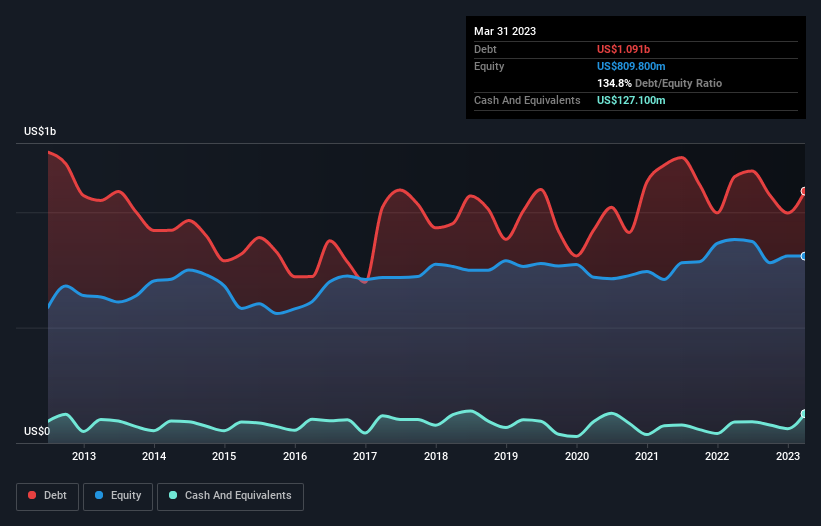

You can click the graphic below for the historical numbers, but it shows that ACCO Brands had US$1.09b of debt in March 2023, down from US$1.15b, one year before. On the flip side, it has US$127.1m in cash leading to net debt of about US$964.3m.

How Healthy Is ACCO Brands’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that ACCO Brands had liabilities of US$504.4m due within 12 months and liabilities of US$1.48b due beyond that. On the other hand, it had cash of US$127.1m and US$303.8m worth of receivables due within a year. So its liabilities total US$1.55b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the US$496.4m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we’d watch its balance sheet closely, without a doubt. At the end of the day, ACCO Brands would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

ACCO Brands’s debt is 4.7 times its EBITDA, and its EBIT cover its interest expense 3.5 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Even worse, ACCO Brands saw its EBIT tank 22% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine ACCO Brands’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, ACCO Brands recorded free cash flow worth 69% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

On the face of it, ACCO Brands’s EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Overall, it seems to us that ACCO Brands’s balance sheet is really quite a risk to the business. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say. There’s no doubt that we learn most about debt from the balance sheet.