Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Southwestern Energy Company (NYSE:SWN) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Southwestern Energy’s Debt?

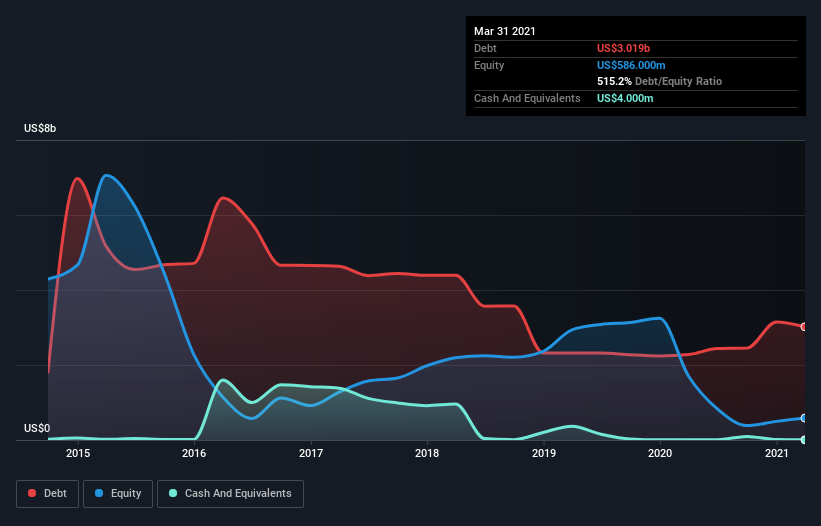

The image below, which you can click on for greater detail, shows that at March 2021 Southwestern Energy had debt of US$3.02b, up from US$2.28b in one year. Net debt is about the same, since the it doesn’t have much cash.

How Strong Is Southwestern Energy’s Balance Sheet?

We can see from the most recent balance sheet that Southwestern Energy had liabilities of US$1.37b falling due within a year, and liabilities of US$3.29b due beyond that. Offsetting this, it had US$4.00m in cash and US$400.0m in receivables that were due within 12 months. So its liabilities total US$4.26b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company’s US$3.26b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Weak interest cover of 0.18 times and a disturbingly high net debt to EBITDA ratio of 8.4 hit our confidence in Southwestern Energy like a one-two punch to the gut. This means we’d consider it to have a heavy debt load. Worse, Southwestern Energy’s EBIT was down 97% over the last year. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Southwestern Energy’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Southwestern Energy burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

On the face of it, Southwestern Energy’s conversion of EBIT to free cash flow left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. And furthermore, its net debt to EBITDA also fails to instill confidence. It looks to us like Southwestern Energy carries a significant balance sheet burden. If you harvest honey without a bee suit, you risk getting stung, so we’d probably stay away from this particular stock. When analysing debt levels, the balance sheet is the obvious place to start.