Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that ON Semiconductor Corporation (NASDAQ:ON) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

What Is ON Semiconductor’s Debt?

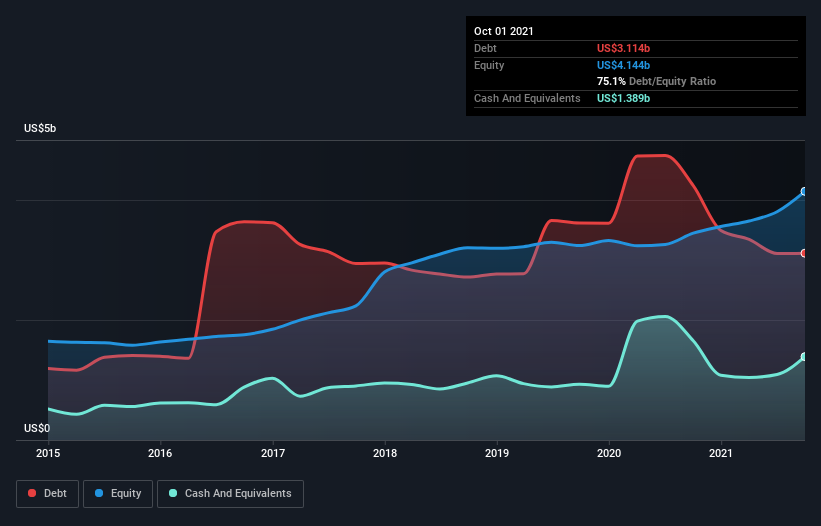

The image below, which you can click on for greater detail, shows that ON Semiconductor had debt of US$3.11b at the end of October 2021, a reduction from US$4.24b over a year. However, because it has a cash reserve of US$1.39b, its net debt is less, at about US$1.72b.

How Strong Is ON Semiconductor’s Balance Sheet?

According to the last reported balance sheet, ON Semiconductor had liabilities of US$1.44b due within 12 months, and liabilities of US$3.35b due beyond 12 months. Offsetting these obligations, it had cash of US$1.39b as well as receivables valued at US$720.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.69b.

Since publicly traded ON Semiconductor shares are worth a very impressive total of US$26.7b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

ON Semiconductor has net debt of just 1.0 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 7.6 times, which is more than adequate. Better yet, ON Semiconductor grew its EBIT by 172% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if ON Semiconductor can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, ON Semiconductor recorded free cash flow worth 75% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Happily, ON Semiconductor’s impressive EBIT growth rate implies it has the upper hand on its debt. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Zooming out, ON Semiconductor seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity.