The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Avid Bioservices, Inc. (NASDAQ:CDMO) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Avid Bioservices Carry?

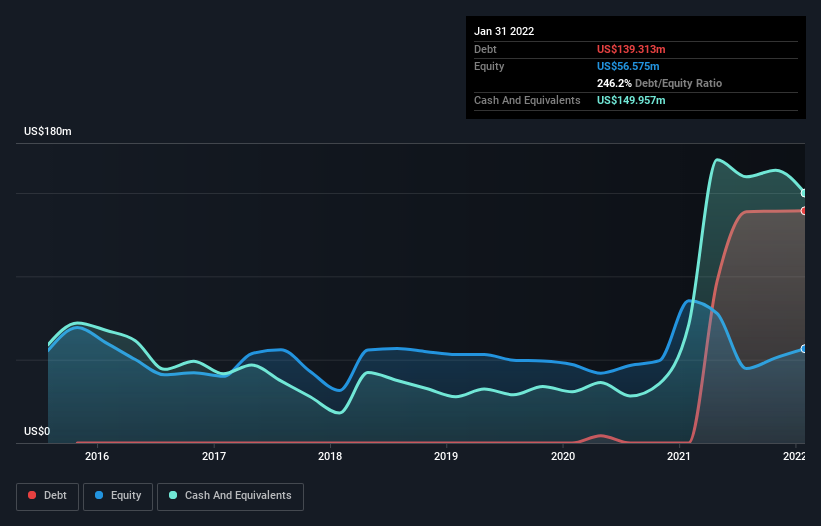

The image below, which you can click on for greater detail, shows that at January 2022 Avid Bioservices had debt of US$139.3m, up from none in one year. But it also has US$150.0m in cash to offset that, meaning it has US$10.6m net cash.

How Healthy Is Avid Bioservices’ Balance Sheet?

The latest balance sheet data shows that Avid Bioservices had liabilities of US$77.3m due within a year, and liabilities of US$180.2m falling due after that. Offsetting these obligations, it had cash of US$150.0m as well as receivables valued at US$31.4m due within 12 months. So it has liabilities totalling US$76.2m more than its cash and near-term receivables, combined.

Since publicly traded Avid Bioservices shares are worth a total of US$850.2m, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Avid Bioservices also has more cash than debt, so we’re pretty confident it can manage its debt safely.

Pleasingly, Avid Bioservices is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 303% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Avid Bioservices’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. While Avid Bioservices has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last two years, Avid Bioservices created free cash flow amounting to 2.7% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing up

We could understand if investors are concerned about Avid Bioservices’s liabilities, but we can be reassured by the fact it has has net cash of US$10.6m. And it impressed us with its EBIT growth of 303% over the last year. So we don’t have any problem with Avid Bioservices’s use of debt. The balance sheet is clearly the area to focus on when you are analysing debt.