Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Comtech Telecommunications Corp. (NASDAQ:CMTL) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Comtech Telecommunications’s Net Debt?

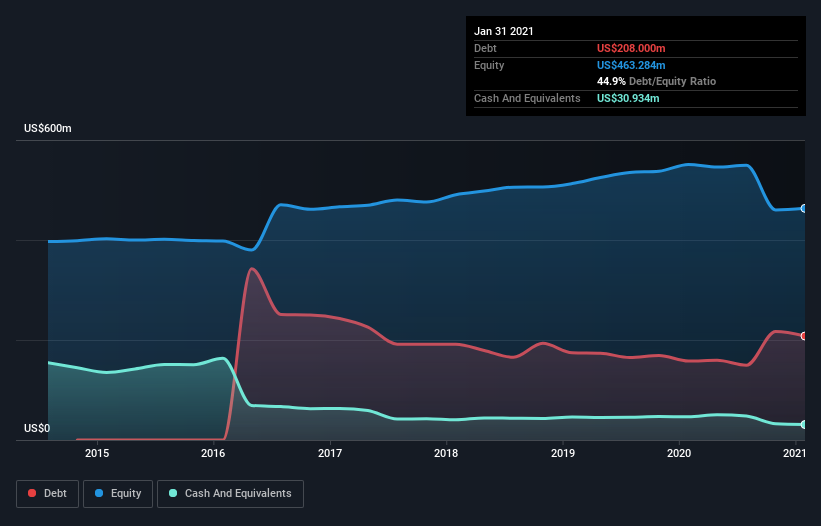

The image below, which you can click on for greater detail, shows that at January 2021 Comtech Telecommunications had debt of US$208.0m, up from US$158.0m in one year. However, because it has a cash reserve of US$30.9m, its net debt is less, at about US$177.1m.

A Look At Comtech Telecommunications’ Liabilities

Zooming in on the latest balance sheet data, we can see that Comtech Telecommunications had liabilities of US$179.7m due within 12 months and liabilities of US$303.6m due beyond that. Offsetting these obligations, it had cash of US$30.9m as well as receivables valued at US$149.9m due within 12 months. So it has liabilities totalling US$302.4m more than its cash and near-term receivables, combined.

Comtech Telecommunications has a market capitalization of US$638.8m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Comtech Telecommunications’s debt is 3.0 times its EBITDA, and its EBIT cover its interest expense 4.3 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Even worse, Comtech Telecommunications saw its EBIT tank 39% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Comtech Telecommunications’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Comtech Telecommunications produced sturdy free cash flow equating to 58% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Mulling over Comtech Telecommunications’s attempt at (not) growing its EBIT, we’re certainly not enthusiastic. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Comtech Telecommunications stock a bit risky. That’s not necessarily a bad thing, but we’d generally feel more comfortable with less leverage. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.