Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Juniper Networks, Inc. (NYSE:JNPR) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Juniper Networks’s Debt?

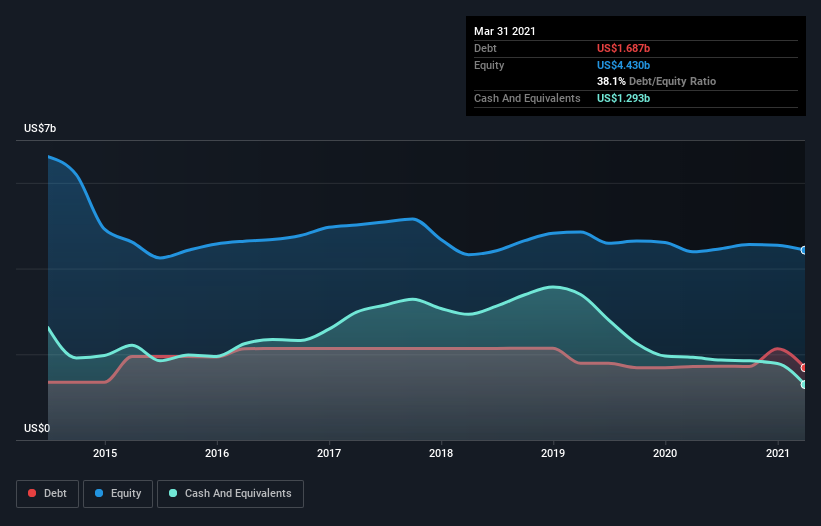

The image below, which you can click on for greater detail, shows that Juniper Networks had debt of US$1.64b at the end of March 2021, a reduction from US$1.71b over a year. On the flip side, it has US$1.29b in cash leading to net debt of about US$344.0m.

How Strong Is Juniper Networks’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Juniper Networks had liabilities of US$1.61b due within 12 months and liabilities of US$2.67b due beyond that. Offsetting these obligations, it had cash of US$1.29b as well as receivables valued at US$758.9m due within 12 months. So its liabilities total US$2.23b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Juniper Networks is worth US$9.11b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With net debt sitting at just 0.52 times EBITDA, Juniper Networks is arguably pretty conservatively geared. And it boasts interest cover of 9.8 times, which is more than adequate. But the other side of the story is that Juniper Networks saw its EBIT decline by 8.2% over the last year. If earnings continue to decline at that rate the company may have increasing difficulty managing its debt load. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Juniper Networks’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Juniper Networks actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Juniper Networks’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But, on a more sombre note, we are a little concerned by its EBIT growth rate. Looking at all the aforementioned factors together, it strikes us that Juniper Networks can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.