Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Horizon Therapeutics Public Limited Company (NASDAQ:HZNP) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Horizon Therapeutics Carry?

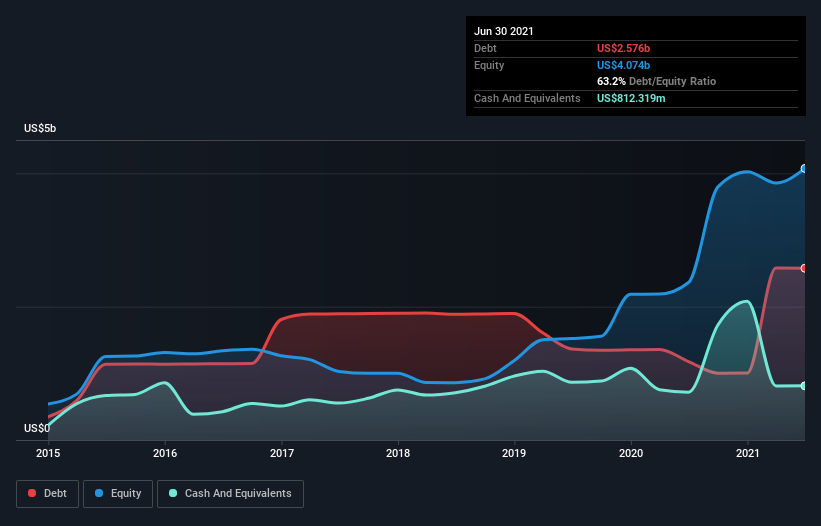

As you can see below, at the end of June 2021, Horizon Therapeutics had US$2.58b of debt, up from US$1.18b a year ago. Click the image for more detail. However, it does have US$812.3m in cash offsetting this, leading to net debt of about US$1.76b.

How Strong Is Horizon Therapeutics’ Balance Sheet?

According to the last reported balance sheet, Horizon Therapeutics had liabilities of US$852.8m due within 12 months, and liabilities of US$3.28b due beyond 12 months. Offsetting this, it had US$812.3m in cash and US$735.4m in receivables that were due within 12 months. So it has liabilities totalling US$2.59b more than its cash and near-term receivables, combined.

Of course, Horizon Therapeutics has a titanic market capitalization of US$25.7b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt to EBITDA of 3.0 Horizon Therapeutics has a fairly noticeable amount of debt. On the plus side, its EBIT was 8.9 times its interest expense, and its net debt to EBITDA, was quite high, at 3.0. Notably, Horizon Therapeutics’s EBIT launched higher than Elon Musk, gaining a whopping 325% on last year. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Horizon Therapeutics can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Horizon Therapeutics actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Horizon Therapeutics’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But truth be told we feel its net debt to EBITDA does undermine this impression a bit. Zooming out, Horizon Therapeutics seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity.