The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Ramaco Resources, Inc. (NASDAQ:METC) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

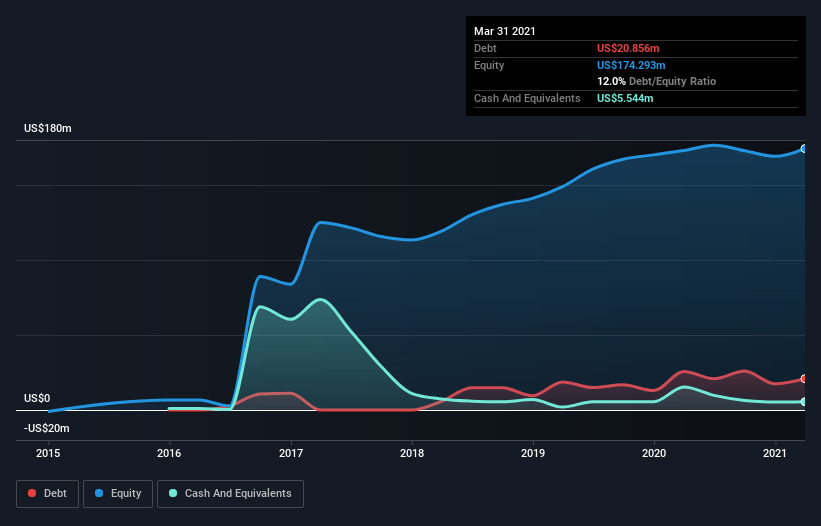

What Is Ramaco Resources’s Net Debt?

As you can see below, Ramaco Resources had US$20.7m of debt at March 2021, down from US$25.6m a year prior. However, it does have US$5.54m in cash offsetting this, leading to net debt of about US$15.2m.

How Healthy Is Ramaco Resources’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Ramaco Resources had liabilities of US$33.3m due within 12 months and liabilities of US$33.4m due beyond that. Offsetting this, it had US$5.54m in cash and US$21.7m in receivables that were due within 12 months. So it has liabilities totalling US$39.4m more than its cash and near-term receivables, combined.

Of course, Ramaco Resources has a market capitalization of US$265.0m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Ramaco Resources can strengthen its balance sheet over time.

Over 12 months, Ramaco Resources made a loss at the EBIT level, and saw its revenue drop to US$170m, which is a fall of 21%. That makes us nervous, to say the least.

Caveat Emptor

While Ramaco Resources’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. To be specific the EBIT loss came in at US$19m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$12m in negative free cash flow over the last twelve months. So suffice it to say we do consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt.