David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Workday, Inc. (NASDAQ:WDAY) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Workday’s Debt?

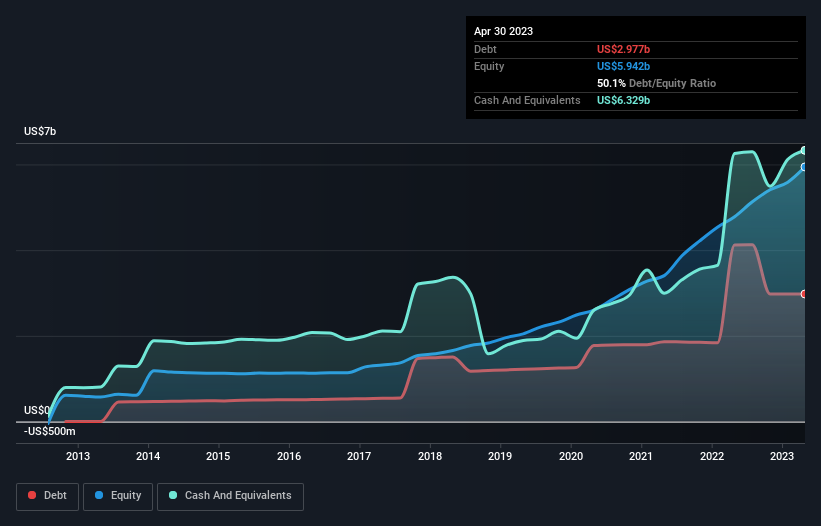

As you can see below, Workday had US$2.98b of debt at April 2023, down from US$4.12b a year prior. But on the other hand it also has US$6.33b in cash, leading to a US$3.35b net cash position.

How Strong Is Workday’s Balance Sheet?

The latest balance sheet data shows that Workday had liabilities of US$4.04b due within a year, and liabilities of US$3.27b falling due after that. Offsetting these obligations, it had cash of US$6.33b as well as receivables valued at US$1.09b due within 12 months. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

This state of affairs indicates that Workday’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$56.0b company is struggling for cash, we still think it’s worth monitoring its balance sheet. Simply put, the fact that Workday has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Workday’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Workday reported revenue of US$6.5b, which is a gain of 20%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Workday?

Although Workday had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$1.1b. So although it is loss-making, it doesn’t seem to have too much near-term balance sheet risk, keeping in mind the net cash. We’ll feel more comfortable with the stock once EBIT is positive, given the lacklustre revenue growth. There’s no doubt that we learn most about debt from the balance sheet.