Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Waste Management, Inc. (NYSE:WM) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Waste Management’s Debt?

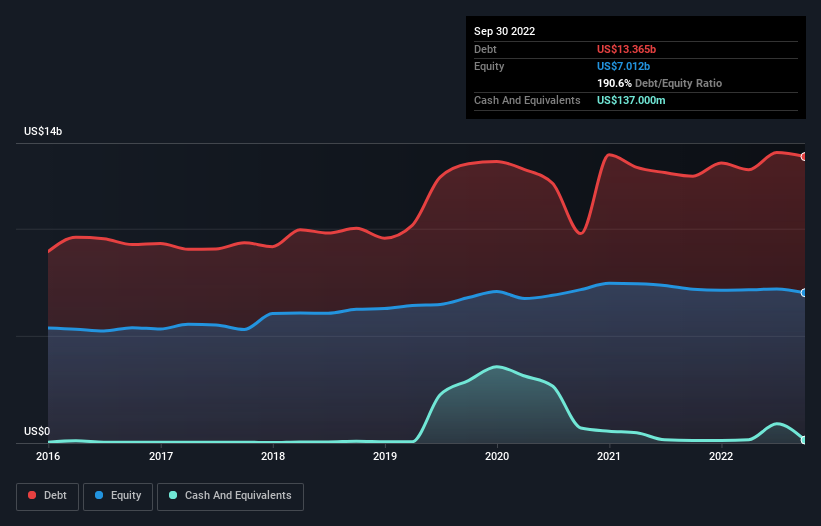

As you can see below, at the end of September 2022, Waste Management had US$13.4b of debt, up from US$12.5b a year ago. Click the image for more detail. Net debt is about the same, since the it doesn’t have much cash.

How Strong Is Waste Management’s Balance Sheet?

The latest balance sheet data shows that Waste Management had liabilities of US$3.83b due within a year, and liabilities of US$19.0b falling due after that. Offsetting these obligations, it had cash of US$137.0m as well as receivables valued at US$2.68b due within 12 months. So it has liabilities totalling US$20.0b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Waste Management has a huge market capitalization of US$69.7b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Waste Management’s net debt of 2.5 times EBITDA suggests graceful use of debt. And the fact that its trailing twelve months of EBIT was 9.5 times its interest expenses harmonizes with that theme. If Waste Management can keep growing EBIT at last year’s rate of 11% over the last year, then it will find its debt load easier to manage. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Waste Management can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Waste Management produced sturdy free cash flow equating to 75% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Happily, Waste Management’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. But truth be told we feel its net debt to EBITDA does undermine this impression a bit. Taking all this data into account, it seems to us that Waste Management takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. The balance sheet is clearly the area to focus on when you are analysing debt.