Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Public Service Enterprise Group Incorporated (NYSE:PEG) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Public Service Enterprise Group’s Debt?

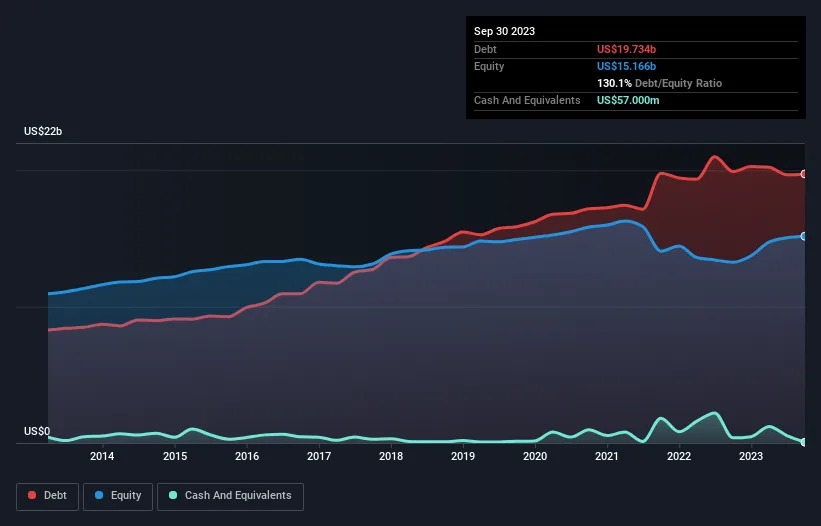

As you can see below, Public Service Enterprise Group had US$19.7b of debt, at September 2023, which is about the same as the year before. You can click the chart for greater detail. And it doesn’t have much cash, so its net debt is about the same.

How Healthy Is Public Service Enterprise Group’s Balance Sheet?

The latest balance sheet data shows that Public Service Enterprise Group had liabilities of US$5.19b due within a year, and liabilities of US$29.2b falling due after that. On the other hand, it had cash of US$57.0m and US$1.59b worth of receivables due within a year. So it has liabilities totalling US$32.7b more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company’s huge US$30.5b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Public Service Enterprise Group has a debt to EBITDA ratio of 3.8 and its EBIT covered its interest expense 6.1 times. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Pleasingly, Public Service Enterprise Group is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 112% gain in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Public Service Enterprise Group can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Public Service Enterprise Group burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

We’d go so far as to say Public Service Enterprise Group’s conversion of EBIT to free cash flow was disappointing. But at least it’s pretty decent at growing its EBIT; that’s encouraging. We should also note that Integrated Utilities industry companies like Public Service Enterprise Group commonly do use debt without problems. Once we consider all the factors above, together, it seems to us that Public Service Enterprise Group’s debt is making it a bit risky.