David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Ebix, Inc. (NASDAQ:EBIX) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

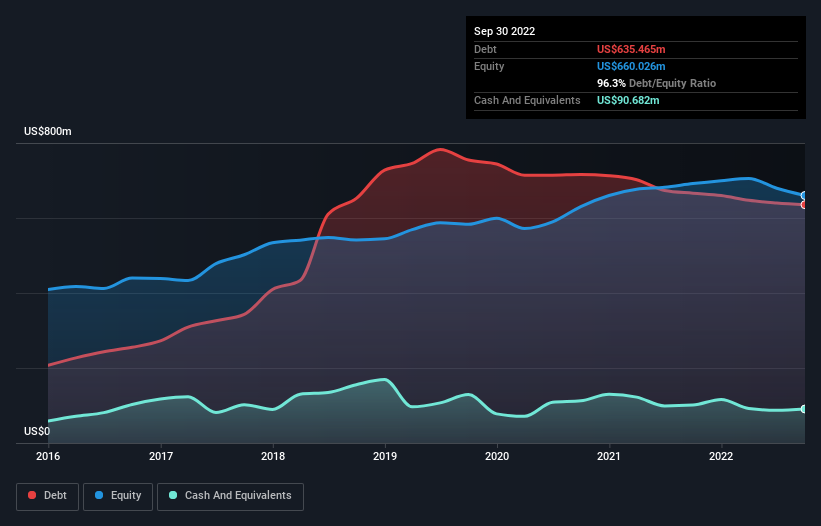

What Is Ebix’s Net Debt?

As you can see below, Ebix had US$635.5m of debt at September 2022, down from US$666.1m a year prior. However, it also had US$90.7m in cash, and so its net debt is US$544.8m.

A Look At Ebix’s Liabilities

According to the last reported balance sheet, Ebix had liabilities of US$805.3m due within 12 months, and liabilities of US$39.6m due beyond 12 months. Offsetting this, it had US$90.7m in cash and US$163.0m in receivables that were due within 12 months. So it has liabilities totalling US$591.2m more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of US$619.6m. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Ebix has a debt to EBITDA ratio of 3.9 and its EBIT covered its interest expense 2.5 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Notably, Ebix’s EBIT was pretty flat over the last year, which isn’t ideal given the debt load. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ebix can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. In the last three years, Ebix’s free cash flow amounted to 46% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

To be frank both Ebix’s level of total liabilities and its track record of covering its interest expense with its EBIT make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Ebix stock a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt.