David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that AxoGen, Inc. (NASDAQ:AXGN) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

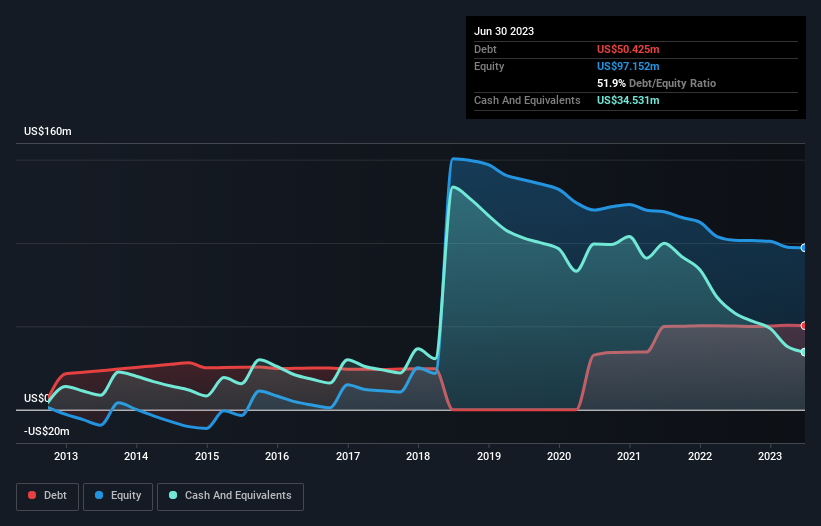

What Is AxoGen’s Net Debt?

The chart below, which you can click on for greater detail, shows that AxoGen had US$50.4m in debt in June 2023; about the same as the year before. However, because it has a cash reserve of US$34.5m, its net debt is less, at about US$15.9m.

How Healthy Is AxoGen’s Balance Sheet?

According to the last reported balance sheet, AxoGen had liabilities of US$23.9m due within 12 months, and liabilities of US$70.6m due beyond 12 months. On the other hand, it had cash of US$34.5m and US$21.6m worth of receivables due within a year. So its liabilities total US$38.4m more than the combination of its cash and short-term receivables.

Given AxoGen has a market capitalization of US$239.8m, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine AxoGen’s ability to maintain a healthy balance sheet going forward.

In the last year AxoGen wasn’t profitable at an EBIT level, but managed to grow its revenue by 15%, to US$148m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Over the last twelve months AxoGen produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable US$25m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair.