Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Upland Software, Inc. (NASDAQ:UPLD) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Upland Software Carry?

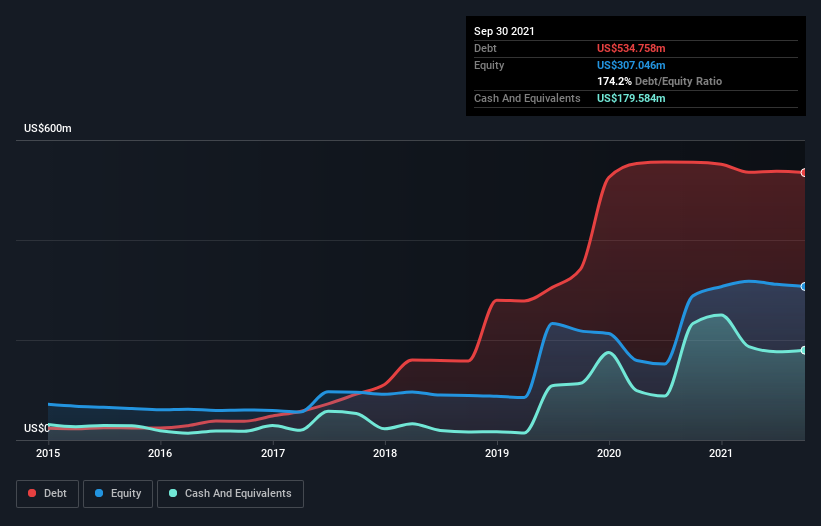

The chart below, which you can click on for greater detail, shows that Upland Software had US$534.8m in debt in September 2021; about the same as the year before. On the flip side, it has US$179.6m in cash leading to net debt of about US$355.2m.

How Healthy Is Upland Software’s Balance Sheet?

We can see from the most recent balance sheet that Upland Software had liabilities of US$145.0m falling due within a year, and liabilities of US$569.7m due beyond that. Offsetting this, it had US$179.6m in cash and US$42.9m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$492.2m.

This is a mountain of leverage relative to its market capitalization of US$593.7m. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Upland Software can strengthen its balance sheet over time.

In the last year Upland Software wasn’t profitable at an EBIT level, but managed to grow its revenue by 8.9%, to US$305m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Upland Software had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at US$3.6m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. We would feel better if it turned its trailing twelve month loss of US$56m into a profit. In the meantime, we consider the stock very risky. When analysing debt levels, the balance sheet is the obvious place to start.