Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Universal Health Services, Inc. (NYSE:UHS) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Universal Health Services’s Net Debt?

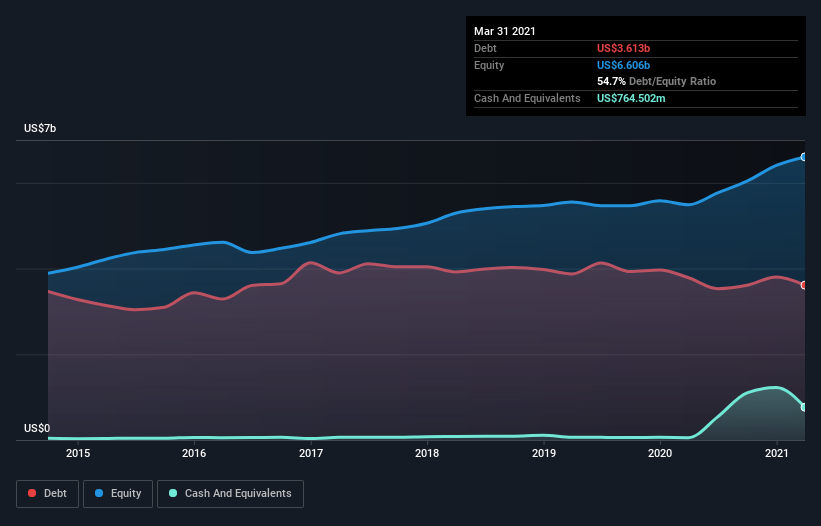

As you can see below, Universal Health Services had US$3.61b of debt at March 2021, down from US$3.79b a year prior. On the flip side, it has US$764.5m in cash leading to net debt of about US$2.85b.

How Strong Is Universal Health Services’ Balance Sheet?

According to the last reported balance sheet, Universal Health Services had liabilities of US$2.24b due within 12 months, and liabilities of US$4.25b due beyond 12 months. On the other hand, it had cash of US$764.5m and US$1.67b worth of receivables due within a year. So it has liabilities totalling US$4.06b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Universal Health Services has a huge market capitalization of US$12.9b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Universal Health Services’s net debt is only 1.5 times its EBITDA. And its EBIT covers its interest expense a whopping 15.6 times over. So we’re pretty relaxed about its super-conservative use of debt. And we also note warmly that Universal Health Services grew its EBIT by 17% last year, making its debt load easier to handle. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Universal Health Services’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Universal Health Services produced sturdy free cash flow equating to 67% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that Universal Health Services’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! We would also note that Healthcare industry companies like Universal Health Services commonly do use debt without problems. Zooming out, Universal Health Services seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. When analysing debt levels, the balance sheet is the obvious place to start.